2020 has been a year that will stand out in the history books. Financial markets have seen their own share of history in 2020, including significant inflection points, both those readily apparent, and those that have existed behind the scenes.

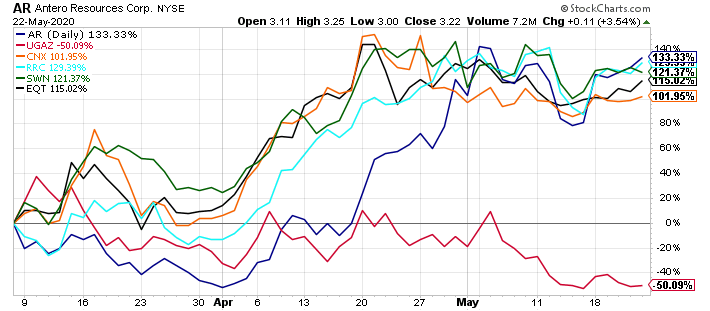

In the energy sector, March 9th, 2020 was a significant inflection point, where many energy equities, including Occidental Petroleum (OXY) declined over 50% in a single trading session, and alternatively, leading natural gas equities, including EQT Corp. (EQT), Cabot Oil & Gas (COG), and Southwestern Energy (SWN) actually finished higher amid the energy carnage, as I chronicled and outlined in the following two public articles.

While natural gas equities have shined in the energy complex in 2020, energy stocks, and value stocks have generally continued to be out-of-favor, however, the inflection point might have been reached on November 9th, 2020.

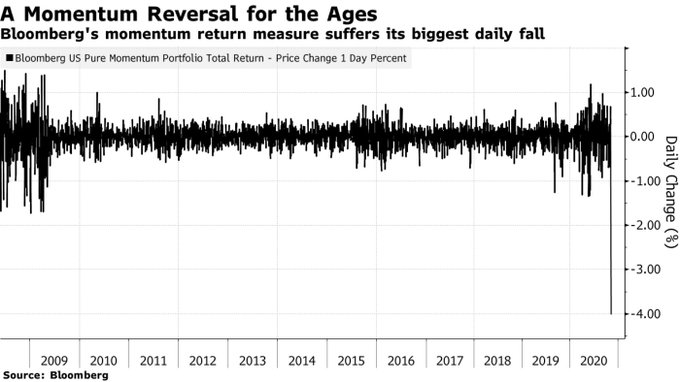

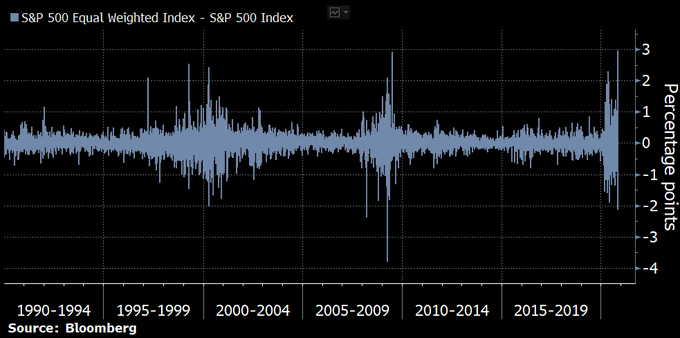

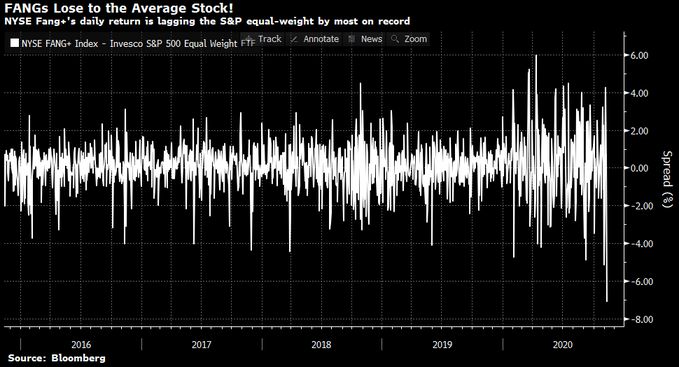

A Record Change In The Relative Performance Of Momentum Stocks Occurred On November 9th, 2020.S&P 500 Equal Weight ETF (RSP) Had Its Best Relative Performance Day Versus SPDR S&P 500 ETF (SPY) Ever On November 9th, 2020!FAANG Stocks Had Worst Relative Performance Day Since Acronym Gained Popularity On November 9th, 2020!

Takeaway Thoughts

Sometimes an inflection point is obvious, hitting an observer over the head, and sometimes it is more discreet, requiring some time to appreciate what has transpired. With energy stocks, which are the fulcrum of the value opportunity, continuing to outperform this past week ending Friday, November 20th, 2020, including the Energy Select SPDR Fund (XLE) rising 5.7%, the SPDR S&P Oil & Gas Exploration & Production ETF (XOP) rising 6.6%, and the VanEck Vectors Oil Services ETF (OIH) rising 10.9%, while the SPDR S&P 500 ETF (SPY) declined 0.8%, and the Invesco QQQ Trust (QQQ) declined 0.2%, market participants may look back to November 9th, 2020, and view it as a line of demarcation between the “Have’s” and the “Have Not’s”.

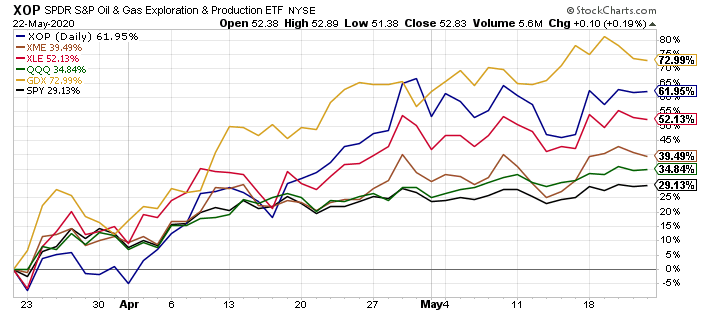

The broader equity market bottomed on March 23rd, 2020, and since then the SPDR S&P 500 Index ETF (SPY) is higher by 29.1%, and the Invesco QQQ Trust (QQQ) is higher by 34.8%, as shown in the chart below.

Somewhat inconspicuously, precious metals equities, as measured by the VanEck Vector Gold Miners ETF (GDX), have risen 73.0% since the March 23rd broader market low, energy equities, as measured by the Energy Select Sector SPDR Fund (XLE) and the SPDR S&P Oil & Gas Exploration & Production ETF (XOP), have risen 52.1% and 62.0%, respectively, from the March 23rd broader market low, and basic material stocks, as measured by the SPDR S&P Metals & Mining ETF (XME), which have risen 39.5% since the March 23rd broader market low.

Said another way, inflation sensitive and economically sensitive equities are quietly outperforming.

At the time of this publication, I was routinely mocked, much as I was in 2008 and 2009, before this happened.

How did I achieve this performance?

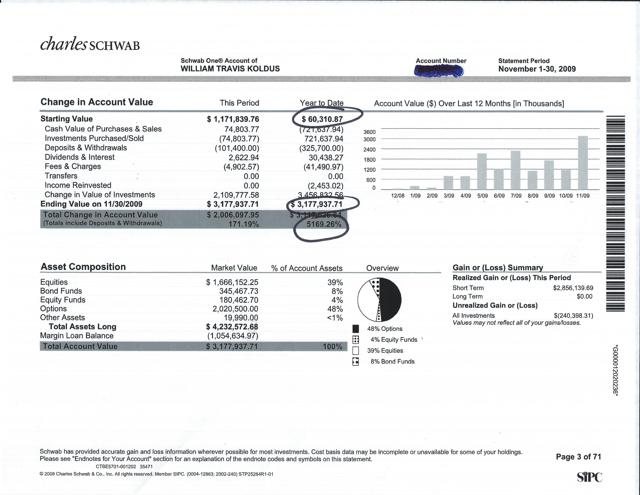

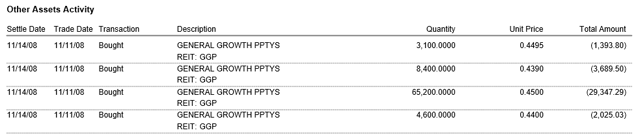

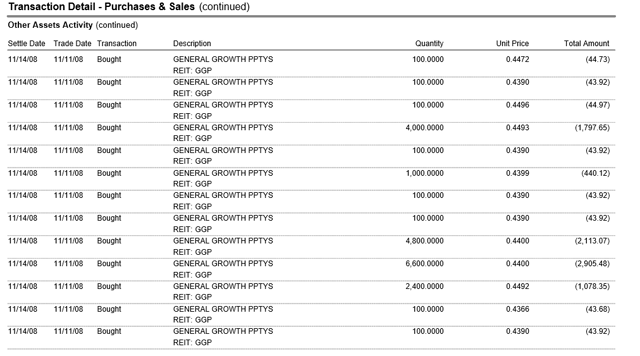

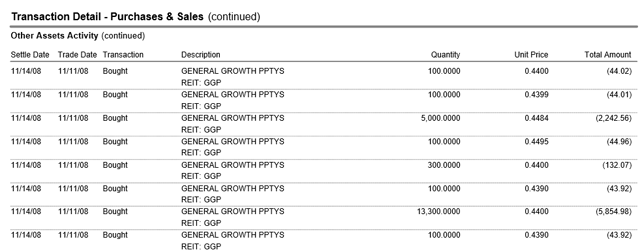

Simply put, it was buying undervalued equities, like General Growth Properties, in November of 2008, that almost nobody else wanted.

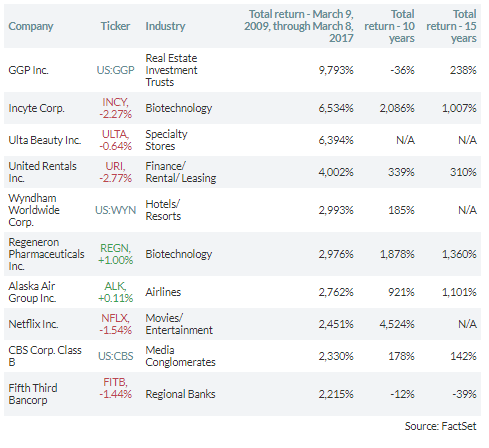

As I have said previously, these purchases, in aggregate, totaled $53,593.71, which was not a big dollar total in aggregate, however, the 120,000 shares were a nice stake in what would become the best performing S&P 500 equity in the bull market, at least through March 10th, 2017, as this CBS MarketWatch article on the bull market turning 8 years old chronicled.

In March of 2018, in the Brookfield Property Partners deal, these shares could be exchanged for $23.50 in cash.

Not a bad return at all, however, the key was to buy into the panic. That is the same thing we have done this time, and now we will see if the proverbial Main Course plays out in front of our eyes.

Best of luck to everyone. Stay healthy, safe, and happy,

I have been waiting for a long time for a set of events to end the virtuous melt-up, fueled by passive and ETF fund flows.

Coronavirus could be the black swan that causes a reversal of these fund flows.

Non-correlated equities with low index representation stand to benefit disproportionately.

Introduction

We are potentially on the verge of an historic capital rotation from growth to value, sparked by black swan catalysts that nobody envisioned a short time ago.

Building on this narrative, on February 6th, 2018, I wrote one of my most popular articles published on Seeking Alpha titled, “Be Prepared For A Crash – Part II“, and in the article, I specifically investigated the lack of price discovery in the markets, as passive, ETF, and dividend growth fund flows were largely price insensitive and valuation insensitive in their endless buying.

Today, that virtuous, seemingly never ending cycle has the potential to work in reverse fashion. In Steven Bregman’s words, all that was needed was a signal event to jump start a golden age for active investors, and we may have one transpiring in real time.

To illustrate this point, I referenced several quotes from Steven Bregman, president and co-founder of Horizon Kinectics, who presented at James Grant’s October 4th, 2016 Investment Conference.

Here is the first set of quotes I referenced:

“A golden age of active investment management awaits only one signal event, Steven Bregman, president and co-founder of Horizon Kinetics, told the Grant’s conference-comers on Oct. 4. A collapse of the index/ETF bubble is that intervening disaster. To hear Bregman tell it, no crash would be so well-deserved

He called the exchange-traded fund excrescence the world’s biggest bubble.

“It has distorted clearing prices in every sort of financial asset in every corner of the globe…,” asserted Bregman. “[I]t has created a massive systemic risk to which everyone who believes they are well diversified in the conventional sense are now exposed.”

I could not agree more with the statement quoted above, and these price distortions have increased at an exponential rate from 2017-2019, and early into 2020, as crowded trades have become more crowded.

Conversely, the “Have Not” equities have been shunned to an even further degree, creating the most bifurcated market that I have seen in my 25 plus years actively investing and speculating.

A Historic Capital Rotation Is On The Horizon

Once passive, ETF, and index fund flows reverse, the disproportionately beneficiary equities, think the leading market capitalization index favorites, are going to be the equities that are hurt most by the reversal of fund flows. Conversely, out-of-favor equities that have been shunned, will actually benefit, as long/short funds reduce gross market exposure, and net buying, at least net relative buying will head to these equities.

On this note, here are the 25 largest components of the SPDR S&P 500 Index ETF (SPY), which have all been buoyed by never ending passive fund flows.

Personally, I think the top weighted companies on this list, which dominate the S&P 500 Index, and the Invesco QQQ Trust ETF (QQQ), have a chance to sell-off dramatically, if a true capital rotation takes hold from growth to value.

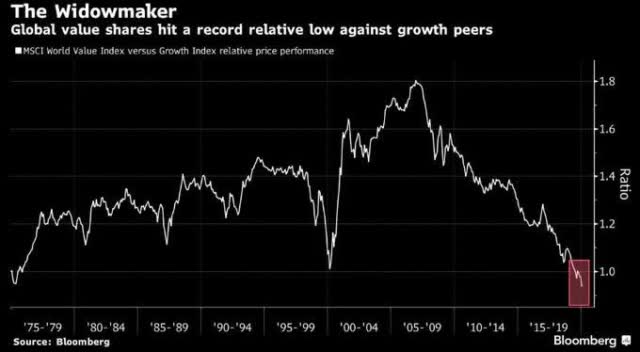

Given the current extended levels of growth versus value, there is a ripe opportunity for an epic price reversal.

Looking at the above, look how steep the price reversal was in 2000-2002, with the growth to value relationship reversing on a dime, and moving straight in the other direction.

Could the same thing happen today?

Yes, is my unequivocal answer, partly because the in-favor investment strategies and trades, think passive, ETF, and dividend growth fund flows, are even more popular today on a relative basis than they were in the late 1990’s, as almost every registered investment advisor in the U.S. has shifted to some form of passive indexing.

Wrapping up, coming from a value investment background, I have seen many of my peers ground to dust, and legendary value investors essentially take their ball and go home. Personally, I have more significant scars from this time frame than any other.

The collective price action and collective investor response is very reminiscent of Julian Robertson closing his Tiger Funds near the exact peak of the 1990-2000 bubble, an investment landscape that had seen Warren Buffett routinely criticized. Of course, this was followed by a massive reversion-to-the-mean trade from 2000-2002, and really 2000-2007, where value investing handily outperformed.

Building on this narrative, during 2000-2002, the S&P 500 Index lost roughly 50% from peak-to-trough, while many value stocks, including REITs, like Realty Income (O), which was loathed at the time, but loved today after roughly two decades of out-performance, surged higher, even with the broader market struggling mightily.

With that last thought in mind, consider what investments are loathed, and loved, today.

In closing, for the value investors that are left today, the odds seem insurmountable, however, the opportunities, particularly on a relative basis, are as big as they have ever been.

To get an idea of how I am positioning for this opportunity, since we are past there, in my opinion, I am offering a 20% discount to membership (I am extending this through February) to “The Contrarian” (past members can also direct message me for a special rate), the lowest price point since the founding members price, where we have a live documented history dating back to late 2015..

Additionally, I am offering a limited time 40% discount for the first 5 new members, repeating a successful promotion from earlier this month (I expect these slots, some of which I view as a stepping stone to “The Contrarian”, to fill up fast as they have done previously) to a host of research options, including a lower price point. To get this offer, go here, and enter coupon code “february 2020” without the quotes.

Reach out with any questions via direct message.

Via my research services, or another avenue, please do your due diligence, and take advantage of what I believe is a historic inflection point,

Disclosure: I am/we are long BAC, C, xom, and short AAPL via put options and spy in a long/short portfolio.

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.