- Resilience is one of the keys to market success.

- It has been a long, difficult stretch, yet there is light at the end of the tunnel.

- Prepare accordingly for the opportunity.

(WTK’s Note: This picture shows how I want to feel after downtrodden, out-of-favor value equities reclaim their rightful mantle of the stock’s markets best performers…actually poor Andy suffered long after this scene…so really I want to feel how he felt upon reaching Zihuatanejo..for more of my take on the Shawshank Redemption and how it applies to investing…read this post).

When I was sixteen, which is now twenty-five years ago, I bought a brand new GMC Sonoma blue pick-up truck, which I drove right until it died on me in an apartment parking lot roughly a decade later.

The blue GMC pick-up truck was partially funded from my paper route, which I had since the age of 9, and partially funded through ongoing work during high school, including as a dishwasher, cook at a restaurant (Schoops in NW Indiana…I could grill a hamburger with the flattened edges to perfection), and as a jack-of-all trades at St. Anthony’s Hospital, with much of my time as a stock boy.

Not that kind of stock boy, but rather actually stocking shelves, though I was already knee-deep in the stock market, actively trading at that time (without the technology comforts, or access to the markets, of today…perhaps that was a good thing).

One night when I was 16, after a long shift cooking, and closing at the restaurant, I was driving home around midnight, on an almost empty four-lane road, and I looked down briefly to adjust the radio.

Before I could look up, a car had veered in front of me, taking a sharp angle to a convenience store, that I had not anticipated.

Boom…my new blue GMC Sonoma pick-up truck rear-ends the car.

Thankfully, nobody is seriously injured.

It is my fault.

I have insurance, but what a night.

To my credit, I took responsibility. The car was fixed, lessons were learned, though I did hit a mailbox driving with my friend Marc Vassallo to work out later that summer, which was the last car accident that I had, hopefully I do not jinx myself with my remembrance.

Note to self. Be careful with oldest children (daughters) as they get close to driving age. They are too close already. Some in our family think they should not drive until 18 or 19, however, there is merit in diving in and learning, though perhaps not in a new car. They need to take risk driving to learn, to be independent, at least that is my view.

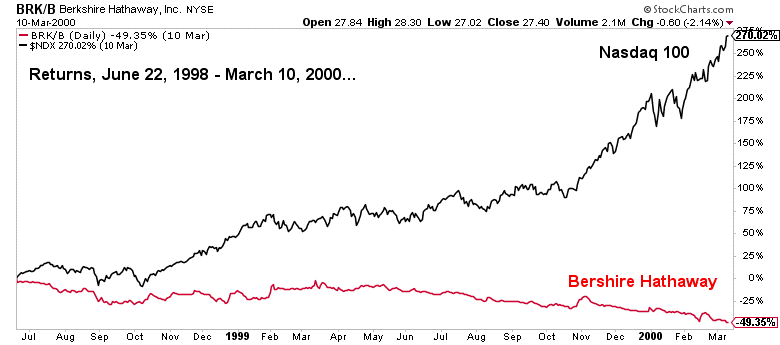

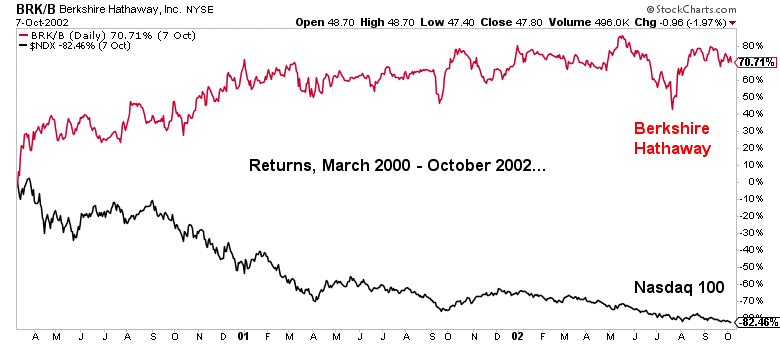

Similar to my accident when I was 16, the last several years, really a long stretch since 2012, with the notable exception of 2016, have been very difficult for my investing style, coming out of nowhere after my most successful stretch trading and investing, as value and concentrated investing approaches have been out-of-favor, and trend following, and passive investment strategies have been dominant in their performance.

Looking back, I have to take responsibility for the wrecks I have caused, meaning investing mistakes, and believe me, these hit home, as I have invested millions and millions of my own capital into what I believe are the best equity return candidates.

Eating my own cooking is the only way I know. It has worked for me before to a degree I never would have imagined, and it has failed me too, even when I was sure of something that ended up being right, but I was still wrong.

That is the cruel irony of markets, and of life too I suppose.

Additionally, I am stubborn to a fault, loyal to a fault, and competitive to a fault, while having the drive and ambition to research something for years if need be, all ingredients for big successes and big failures.

One lesson I have learned in the stock market, after 25 plus years speculating, and investing, is that you have to ask, “what may go wrong?“, even in seemingly the best situation.

Opposite, and not natural when thinking about the aforementioned question above, but a necessary ingredient too, is that investors and speculators must keep in mind “what could go right“.

Looking back on this note, my biggest mistakes in Dollar terms, has been selling something too early, after building a big position, typically in a value equity, and initially thinking I was right, and then taking profits too early.

Hubris and a need to do something are enemies in the stock market. Personally, every time my ego has ballooned, something happens to let out the air.

Patience, and acting when presented with an opportunity, are allies in the stock market.

Most importantly, though, in my opinion, is resilience, and the tenacity, and persistence to stick with an idea.

What is the point of my late night reminiscing and rambling?

It boils down to a couple things. We are all going to make mistakes investing and speculating (and in life too). Sometimes these are big mistakes. When this happens, we have to take responsibility, learn from them, and then, and this is key, not be afraid to take risk.

What is risk anyway right now?

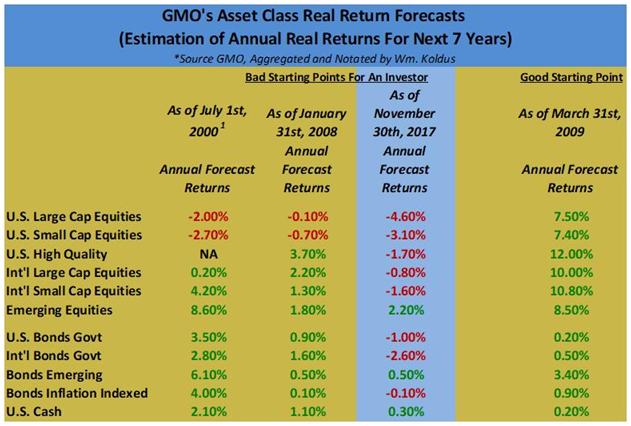

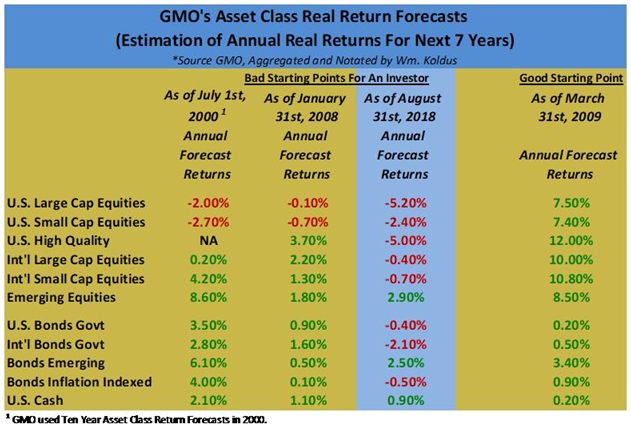

Is somebody fully invested in the stock market very risky? I would say so, given my views on market valuations, which are echoed in this long running table that I have put together that I get laughed at now for posting.

Looking at the table above, the broad U.S. equity market looks historically risky to me, with the caveat that I would have said this, using the same information, for a long time now.

So to me, U.S. equities are historically risky, with strangely many very cheap bargains, however, another person may say someone all in cash is risky.

This question of risk is all in the eye of the beholder, however, I would say after nearly a decade of the “winner’s” winning, there may be more risk in these winning equities that investors, speculators, and long-time holder imagine, and alternatively, there may be a good risk/return reward ratio (say that five times fast) in many of the out-of-favor, downtrodden equities that have generally not participated in the bull market the last decade.

Ironically, many investors would not touch these equities today, and really, who could blame them.

You would have to have the patience of Andy Dufresne, the famous flawed, resilient protagonist in Shawshank Redemption to be interested in many of these downtrodden, out-of-favor equities.

“Not participated”, by the way, is a kind term, as many out-of-favor equities, even some household names, have been crushed, far out of sight of the shiny, roughly decade long bull market in the S&P 500 Index (SPY).

The discussion of where to invest, what is risky, and what is historic opportunity, is a lively topic at The Contrarian, which is my premium research service platform on Seeking Alpha.

I am biased, of course, but I think we have the best group of investors and traders anywhere, seasoned by nearly three years of commentary for some members, with many members actively contributing their unique perspectives to a robust Live Chat discussion on a daily basis, particularly when volatility surfaces.

Right now, we have an open free trial at The Contrarian, so if you have ever had an interest in test driving our group, now is a good time.

From my perspective, as I said in my blog post yesterday, it would be worth taking a look, simply to view the Live Chat dialogue.

The price point of The Contrarian is a little steep, coming in as one of the more expensive services in SA’s Marketplace.

Over the years, I have had quite a few requests for a lower-priced, more streamlined research product, and over the last several months, I have slowly put together a more traditional research newsletter.

To celebrate this official launch, which includes a deep-dive research report on what I believe is an extremely timely equity (delivered via email upon membership), I am offering a limited time $299 annual membership for the first 100 members. To get this discounted price, simply use the coupon code “first100”.

Ultimately, I think we are now at a major inflection point in the financial markets, which has been ongoing in slow motion for three years, but which could suddenly accelerate. Being different, being contrarian, has been extremely painful for a long time now, however, resilience and persistence, two necessary qualities for success in contrarian investing, in my opinion, are leading to what I believe is an upcoming golden age for active investors.

Hope you enjoyed my trip down memory lane as much as I did (I still remember running stairs every morning at the high school football field trying to build up calf strength to dunk a basketball…different worries today),

WTK

Disclosure: I am/we are short spy as a market hedge, and have put more money into commodity equities that i ever should have, yet the opportunity remains IMO.

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.