Earlier today, a public article I posted about Antero Resources (AR) was published on Seeking Alpha. You can find it under this title & link, “Antero Resources Is A Generational Buy: Dispelling The Myth Of Antero As A High-Cost Producer“. While writing this article, and spending a lot of time researching commodity equities, and more specifically energy equities the past 5 years, really the past 7 years, that has snowballed to an almost obsession now, due to the inherent undervaluations, I have slowly worked to the conclusion that most market participants have become over obsessed with quality and/or perceived quality.

What do I mean by this?

In the case of Antero, almost all long/short fund managers I know, are long Cabot Oil & Gas, and short Antero. The relentless price action in favor of this trade, has essentially eradicated valuation sensitive and price sensitive money out the door.

Building on this narrative, the Darwinian survival funnel of the markets, has led almost all investors to the same securities the past decade, a ending place where quality and dividends are praised above all, and the perceived quality, and sustainability of dividend growth, and/or yield is worshiped.

The end result of this process is a bubble that is bigger than the late 1990’s bubble, more pervasive, and more driven by longer-term sovereign interest rates than anything else.

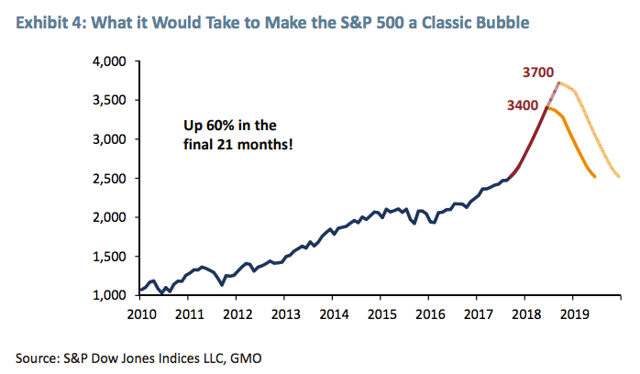

Looking back to 2018, GMO laid out a path for a classic bubble for the S&P 500 Index (SPY), and we are there, as the following graphic illustrates.

Looking at the above, once we peak, and roll-over, the path is frightening, something many market participants have some how forgotten following 2007-2009, and 2000-2002.

Really, though, it is worse than that, as yield-oriented investors have been pushed out the risk curve, and the perceived quality equities, namely the dividend payers, have become essentially the longest duration bonds.

I wrote about this with my Procter & Gamble (PG) public article, titled, “Procter & Gamble Is Historically Overpriced.”

Jumping straight to the punch line, what happens when almost all market participants embrace quality, perceived quality, and are piled into essentially the longest duration assets, chasing yield, when longer-term interest rates rise?

Who is prepared for this?

Will this lead to the historic bifurcation between the “Have’s” and the “Have Not’s” being closed?

My vote is a resounding yes!