- Passive investing, and ETF investing, have dominated the last decade.

- These unsustainable investing trends have created giant price distortions.

- The next decade will be extremely lucrative for active investors and we are at an inflection point today.

(Travis’s Opening Note: This article was originally authored and published on September 21st, 2017, and it remains a “foundation article”, in my opinion, for my current investment stance, and it one of my favorite articles that I have authored. It is being republished today, on 10/23/2018, to launch a new series category, which will be titled “Author’s Highlighted Posts”.)

“A 60:40 allocation to passive long-only equities and bonds has been a great proposition for the last 35 years,” …”We are profoundly worried that this could be a risky allocation over the next 10.”

Sanford C. Bernstein & Company Analysts (January 2017)

“Be stubborn on vision and flexible on journey”

Noramay Cadena

Life and investing are long ballgames.”

Julian Robertson

Opening Note From WTK

When I worked at Oxford Financial Group, Limited, which was, and remains one of the largest RIA’s in the United States, I was hired by the CIO, Howard Harpster, who was the former head of BP Amoco’s (BP) pension plan. Howard was an intelligent, calculated risk-taker who cultivated relationships in the then opaque, and relationship-based, private equity, private real estate, and hedge fund arenas.

Howard eventually returned to his native Texas, which is near and dear to my heart, as I have many close relatives and friends in Texas, to sort through a family estate, and then take the role of CIO at the Texas Children’s Hospital.

Oxford conducted an executive search, on which I served a role, and narrowed the candidates for CIO to two individuals, ultimately hiring their current CIO in roughly late 2006 or early 2007.

The new CIO, who came from a background at Okabena, which was the family office created by the founding family of Target (TGT), embraced passive investing.

This firmly contrasted with my belief that the markets were not efficient, and we had a rousing discussion and debate for several years, both between the CIO and our broader investment strategy group, which was composed of four key decision makers, including myself, before I ultimately resigned, with good relationships in-tact, to start my investment firm in February of 2009.

At the time, I was full of confidence, as I had made money in 2008, when most investors and speculators lost money, and then I procured a small fortune, at least for me, from timely investments made in 2008 & 2009.

In the middle of 2008 and 2009, I thought it was a dream environment for active investors, and I could not see how the passive investment craze, that characterized the market’s rise from 2003-2007 could continue.

I was spectacularly wrong with this prediction.

Passive investing has dominated the past decade, making the shift to passive investments from 2003-2007 look like a blip on a long-term chart.

This has driven many active managers out of the investment industry (Travis’s Updated Note 10/23/2018: This purge has continued into 2018), accelerating the dispersion between passive investors and value investors, which has resulted in hedge fund closures, the decline of once prominent mutual fund families, and the downgrade in reputation to value investing and value investors.

This seemingly never ending, self-reinforcing, investment cycle has resulted in a bi-furcated market, where the favored investments of passive indexes, dividend growth strategies, and popular ETF’s are traded at some of the highest valuations in history, while equities outside these favored strategies trade at some of the lowest valuations in history.

In summary, this has created another dream environment for active investors, which is even better than 2008-2009 time-frame, in my opinion, and a golden age of active investing is right in front of investors and speculators, in my opinion.

We got a taste of this opportunity in 2016, but the market has not made the pendulum shift from passive investing being in-favor to active value investing being in-favor easy. In fact, 2017 has been one of the most difficult, if not the most difficult years, of my investment career, thus far, but that should not take away from the scope, or magnitude, of the opportunity that is at hand.

Someday in the near-future, it is my prediction that investors will rue the fact that their equities are part of the benchmark indexes, and popular ETF strategies. Thus, we sit on the cusp of a historic inflection point. On this note, I came across a past issue of Grant’s Interest Rate Observer, from last October, about a week ago, that reinforced this point, and I wanted to write something about it, so here is that observation as part of my Investment Philosophy series.

Selected Prior Member Articles Of Interest On Investment Philosophy & Related Topics

Selected prior articles of interest for members on investment philosophy, market history, and portfolio strategy include:

Investing Philosophy – Abandoning Ship & Capitulation – 8/3/2017

Investment Philosophy – Identifying A Good Opportunity Is Only Half The Battle – 7/16/2017

Investing Philosophy – Staying Focused Is Hard To Do – 5/27/2017

Market Historian – What Happens When The Fed Raises Rates – 3/16/2017

Investment Philosophy – The Fallacy That You Always Need To Be Fully Invested – 2/2/2017

A Matter Of Perspective – Commodities & Commodity Stocks – 1/6/2017

Interview Series – Part II Of WTK’s Take On Edward Chancellor’s View With A Focus On Precious Metal Equities – 12/15/2016

Interview Series – WTK’s Take On Edward Chancellor’s View On “Intelligent Contrarian Investing” – 11/21/2016

Investment Philosophy For The Contrarian Subscribers – A Take From John Hempton @ Bronte Capital – 10/20/2016

The Contrarian’s Top-Ten Lists & Thoughts On Portfolio Strategy – 9/29/2016

Reviewing Lucas White’s And Jeremey Grantham’s Research On Commodity Stocks & A Market Note From WTK – 9/9/2016

Working Investment Thesis

It is my belief that we are in the final innings of the bull market that began in March of 2009, with bonds topping now, then stocks, and then commodities.

The Inspiration

Last week, I was reading, and researching, and I came across an October 14th, 2016 issue of Grant’s Interest Rate Observer, which was a recap of a presentation that Steven Bregman gave at Grant’s October Investment Conference.

I have been a subscriber to Grant’s Interest Rate Observer, and I am a fan of James Grant, who was born in New York City, but attended undergraduate college at Indiana University. Mr. Grant has maintained ties to Indiana, including speaking as a guest speaker at the CFA Society of Indianapolis functions, which I have been involved with as a current member and past board member (I have also been a member of the Chicago CFA Society where Grant’s work has been featured).

This particular issue caught my eye, because it delved into the index/ETF bubble, which has been a topic that I have been writing about, and which I have been thinking about a lot lately.

A Passive Investing ETF Bubble

The opening paragraph describes the topic up for discussion, and the second paragraph spells out the views of Steven Bregman, president and co-founder of Horizon Kinectics, who presented at Grant’s October 4 th, 2016 Investment Conference, and like the famous line from Jerry Maguire, the presentation had me at hello.

Specifically, here is the opening paragraph and then the second paragraph, and then a screen shot that captures the broader discussion.

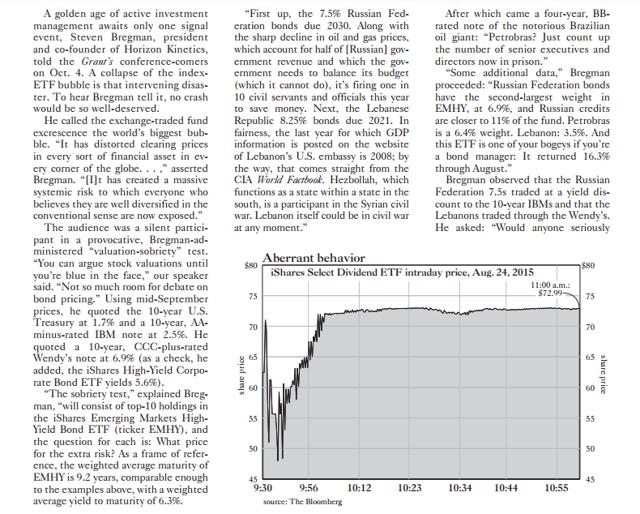

“A golden age of active investment management awaits only one signal event, Steven Bregman, president and co-founder of Horizon Kinetics, told the Grant’s conference-comers on Oct. 4. A collapse of the index/ETF bubble is that intervening disaster. To hear Bregman tell it, no crash would be so well-deserved

He called the exchange-traded fund excrescence the world’s biggest bubble. “It has distorted clearing prices in every sort of financial asset in every corner of the globe…,” asserted Bregman. “[I]t has created a massive systemic risk to which everyone who believes they are well diversified in the conventional sense are now exposed.”

Re-reading this piece, the amazing thing to be is that the passive investing/ETF bubble appeared to peak in 2016, yet roughly a full year later, the excesses have only been amplified.

No Factor For Valuation = No Price Discovery

The crux of Bregman’s case, and my argument too, is illustrated on page 2 of the linked report. In these paragraphs, he deconstructs the iShares Emerging Market Bonds High Yield ETF (EMHY), and in doing so, he exposed the flaws of indexing, particularly when accomplished through ETF investing. Here is a highlighted portion that I think makes a convincing point.

“By operation of law,” Bregman went on, “new money in EMHY is allocated based on float. In other words, the more debt a nation issues, the greater the allocation to its bonds because it has a greater capitalization. Petrobras (PBR) issues more bonds: greater index weight. Yes. The allocations must be done promptly and according to their precise index weights.

“There is no factor in the algorithm for valuation,” our speaker noted. “No analyst at the ETF organizer—or at the Pension Fund that might be investing—who is concerned about it; it’s not in the job description. There is, really, no price discovery. And if there’s no price discovery, is there really a market? In which case, what is EMHY really worth?

“This is about artificial supply-and demand pressures. Now, take this exercise and apply it to the equity indexes. That’s what’s going on. It’s just tougher to debate.”

The emphasis added through formatting was mine, because that is what is going on in the investment management industry. As the former second CIO I worked under at Oxford aptly discovered, probably from “career threatening” mistakes at his prior CIO position at Okabena, there is no reason to take “career risk” when everybody is embracing the same way of investing, namely passive investing, and investing through ETF’s.

Building on this narrative, active investors, particularly active value investors, who were steamrolled from their purchases of financials and real estate equities in 2008 and 2009, negating their typical out-performance in bear markets, have been unable to serve as a check-and-balance to the “blind” passive money, because they have rapidly gone extinct.

Ultimately, this has harmed price discovery and further distorted valuations.

The ETF Divide

During the conference, Bregman highlighted how ETF’s have influenced stock valuations. One specific example that stands out, and was illustrated, was the impact of ETF’s on Exxon Mobil (XOM). Here are the paragraphs discussing its valuation and price performance from 2013-2016.

“Bregman lingered for a while on Exxon, a kind of ETF Swiss Army knife: “Aside from being 25% of the iShares U.S. Energy ETF, 22% of the Vanguard Energy ETF, and so forth, Exxon is simultaneously a Dividend Growth stock and a Deep Value stock. It is in the USA Quality Factor ETF and in the Weak Dollar U.S. Equity ETF. Get this: It’s both a Momentum Tilt stock and a Low Volatility stock. It sounds like a vaudeville act.”

Bregman proposed a mind experiment: “Say in 2013, on a bench in a train station, you came upon a page torn from an ExxonMobil financial statement that a time traveler from 2016 had inadvertently left behind. There it is before you: detailed, factual knowledge of Exxon’s results three years into the future. You’d know everything except, like a morality fable, the stock price: oil prices down 50%, revenue down 46%, earnings down 75%, the dividend-payout ratio almost 3x earnings. If you shorted, you would have lost money”—because the financial statement didn’t mention the coming bifurcation of the stock market that Bregman called the “ETF divide.”

On one side of the line are the anointed ETF constituent securities; on the other side is everything else.”

Again, the emphasis added was mine, as the impact of ETF investing has been particularly pronounced in the commodities sector, and specifically the energy sector.

The larger market capitalization companies that have dominated the energy ETF’s, notably Exxon and Chevron (CVX), have relatively flourished while most of the mid-capitalization and smaller capitalization equities have been in one of the worst energy equity bear markets in modern market history.

Thus, even relatively large exploration and production companies, like Chesapeake Energy (CHK), and Southwestern Energy (SWN), which are the second and third-largest natural gas producers in the United States, have been cast aside due, in part, to their market capitalization’s, which shrink further as they are not included in the exalted passive indexes and chosen ETFs.

Risk Is Misinterpreted

From my writing, you can already probably tell how much I enjoyed this presentation, and the corresponding write-up.

Here is another nugget, via several paragraphs about risk, specifically related to the REIT sector, think the Vanguard REIT ETF (VNQ), or the iShares U.S. Real Estate ETF (IYR), that I think will hit home for many investors.

“Now came a question: “So how do they—the big ‘they’—address this risk?”

And an answer: “In the financial realm, risk has come to be measured by historical price volatility. Consequently, enormous effort is devoted to finding low-volatility sectors with sufficient liquidity. The most prominent statistic for volatility is beta. Go to Yahoo Finance, type in ‘IBM,’ (IBM) and there, front and center alongside price, market cap and dividend yield, is beta.

“Let’s examine this,” Bregman went on. “The iShares REIT ETF (IYR), with a 2.8% yield—which I personally see as 35x earnings—has a beta of 0.72. That is low-risk by definition. But which beta should be used for that definition? The beta for the three years through August 2016? Why not the beta for the three years to March 2007?

“Because the beta at the end of March 2007 was even better—an incredibly low 0.3—only 30% of the volatility of the S&P 500. By February 2009, two years later, the ETF fell 90%, and even Simon Property Group (SPG) shares fell almost 70%, while the S&P (SPY) fell about 46%.”

The problems that we had evaluating risk in 2007 are even worse today, in my opinion, as correlations are higher, and the amount of listed equities in the United States has shrunk by roughly half.

In summary, the accelerated adoption of passive investing and ETF investing has heightened risks, but investors and speculators do not realize this, because volatility in the markets has been so low, and the lack of draw-downs has provided and eerie calm and complacency that supersedes the 2007 investing landscape, in my opinion.

The Opportunity

For someone who has spent the past 25 years actively investing and speculating, but who has gone through a very rough period of performance, I can empathize with the following quote from the write-up of the conference.

“So much for life on the sunlit side of the ETF divide. What about life in the darkness? “In the past two years,” said Bregman (Author’s Note: Remember this presentation occurred in October of 2016, but the trends have continued through today, nearly a year later), “the most outstanding mutual fund and holding-company managers of the past couple of decades, each with different styles, with limited overlap in their portfolios, collectively and simultaneously under-performed the S&P 500. We’re talking 10 to 20 percentage points in a given year. There is no precedent for this. It’s never happened before.

“It is important to understand why,” he stated. “Is it really because they invested poorly? In other words, were they the anomaly for under-performing—and is it reasonable to believe that they all lost their touch at the same time, they all got stupid together? Or was it the S&P 500 that was the anomaly for outperforming?”

From my perspective, I agree with the bulk of this commentary, with the exception of the comment about the under-performance by the best money managers. It has happened before, and it happened fairly recently, specifically in 2007 and 2008.

During this time-frame, active managers, particularly value managers, under-performed, as traditional bastions of value, notably financial stocks, suffered the worst declines.

I can remember than time-frame clearly, and what I remember is that very few analysts and investors could value anything, similar to today. It was confusing, and confounding, but it offered substantial opportunity, as does the investing environment today.

When valuations have no anchor, prices can fluctuate wildly. For us, as contrarian investors, that means some of our big losers on the year, or since inception, have the potential to rapidly reverse course, but it is hard for us to realize that right now, as we have been battered by the non-stop declines, constant negative news headlines, and price action that is seemingly negative every day and every week.

Conclusion – Embrace Active Investing & Being Different Than The Indexes

Here are some quotes I highlighted in the article, directly from the presentation, which again occurred in October of 2016, but is even more relevant today, in my opinion, and I wanted to list them again, because they provide a conclusion that practically writes itself.

“He called the exchange-traded fund excrescence the world’s biggest bubble. “It has distorted clearing prices in every sort of financial asset in every corner of the globe…,” asserted Bregman. “[I]t has created a massive systemic risk to which everyone who believes they are well diversified in the conventional sense are now exposed.”

“There is no factor in the algorithm for valuation,” our speaker noted. “No analyst at the ETF organizer—or at the Pension Fund that might be investing—who is concerned about it; it’s not in the job description. There is, really, no price discovery. And if there’s no price discovery, is there really a market? In which case, what is EMHY really worth?”

“This is about artificial supply-and demand pressures. Now, take this exercise and apply it to the equity indexes. That’s what’s going on. It’s just tougher to debate.”

“On one side of the line are the anointed ETF constituent securities; on the other side is everything else.”

“Because the beta at the end of March 2007 was even better—an incredibly low 0.3—only 30% of the volatility of the S&P 500. By February 2009, two years later, the ETF fell 90%, and even Simon Property Group (SPG) shares fell almost 70%, while the S&P (SPY) fell about 46%.”

“It is important to understand why,” he stated. “Is it really because they invested poorly? In other words, were they the anomaly for underperforming—and is it reasonable to believe that they all lost their touch at the same time, they all got stupid together? Or was it the S&P 500 that was the anomaly for outperforming?”

From the presentation, its documentation, and my chronicling, and commentary, it should be clear that the markets have reached extremes (they had already reached these extremes in 2016 but have extended these extremes further in 2017), perhaps beyond any prior valuation extremes in modern market history. Absolute valuations certainly rival 1999, but relative valuations between the “have’s” and the “have not’s” is even more pronounced.

The lack of price discovery, and valuation analysis, which is accelerated in a self-reinforcing cycle by the massive fund flows into passive and ETF investing, has created a market that is ripe for price discovery, which should be a dream environment for active investors.

In summary, simply surviving to get to the price discovery phase has been difficult, however the rewards should be similar in magnitude, and perhaps even greater than the 2008/2009 opportunity, which rivals any period of potential returns in modern market history.

To close, the market has a dividing line today, which is even more pronounced than 2016, and the stock market remains extremely bi-furcated. The opportunity lies on the other side of this dividing line, in sectors, like commodity equities, which have very little weight in indexes. Drilling down further, commodity stocks that reside outside the “halo” of wide-scale ETF ownership, offer return potential that is every bit as good as the depressed financial and real estate shares in the Spring of 2009.

Two Research Services

To get in on the ground floor of this opportunity (yes it is still a ground floor, maybe even lower after energy prices bottomed nearly three years ago in 2016), please consider one of the two following research services.

First, is The Contrarian, where we have a live history that actually captured the past significant inflection point in 2015 & 2016. Members can read through posts from that time, see how out-sized returns were achieved, look at what is similar today, and try to apply those past learning lessons to today’s market environment.

Put simply, I really appreciate our group at The Contrarian, many members who I have come to respect, and I am optimistic that we are all going to do very well together in the year ahead, similar to 2016.

We are always looking for new members that can add profitable ideas, or challenge existing ones, so if you fit this criteria, consider signing up. A fair warning, though, our group is like the Marines, only a few, only the strong, can survive.

Second, I have had quite a few requests for a lower-priced, curated research product, a stepping stone to The Contrarian (our goal is that you try our research at a lower price, make money, and then later upgrade to The Contrarian for the more in-depth, interactive experience), and over the last several months, I have slowly put together a more traditional research newsletter.

To celebrate the second official month of this research product, where the goal is deliver one deep-dive article a month via a PDF emailed report (and I believe there are a lot of once in a generation opportunities today), I am offering a 21% discount off of a much lower annual price point. To get this limited-time discounted price, simply use the coupon code “december”.

Ultimately, I think we are now at a major inflection point in the financial markets, highlighted by the price action in October of 2018, and November of 2018, which has been ongoing in slow motion for three years, but which could suddenly accelerate. Being different, being contrarian, has been extremely painful for over two years now, however, resilience and persistence, two necessary qualities for success in contrarian investing and in life in general, in my opinion, are leading to what I believe is an upcoming golden age for active investors.

If you have any questions, send me a direct message at any time,

Travis

P.S. I have learned over my career that handling disappointment, and taking advantage of the resulting opportunity is a crucial skill for investors and speculators. I cannot tell you how often I am disappointed in the investment markets with price action, yet stubbornness, persistence, and hard work often, but not always, result in a favorable situation, like most things in life.

P.S. II With everyone looking for a price dislocation similar to 2007-2009, look for something different to happen, including a potential pick up in inflation and interest rates, which very few are even considering.