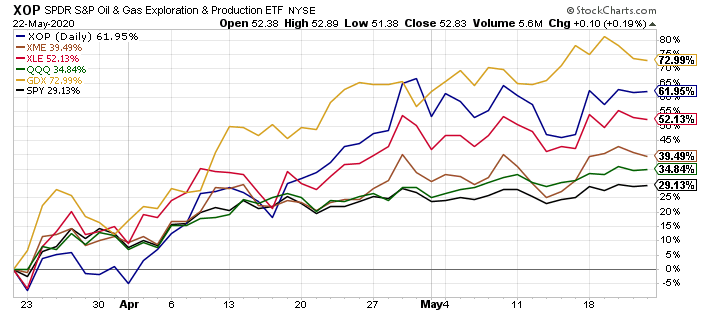

The broader equity market bottomed on March 23rd, 2020, and since then the SPDR S&P 500 Index ETF (SPY) is higher by 29.1%, and the Invesco QQQ Trust (QQQ) is higher by 34.8%, as shown in the chart below.

Somewhat inconspicuously, precious metals equities, as measured by the VanEck Vector Gold Miners ETF (GDX), have risen 73.0% since the March 23rd broader market low, energy equities, as measured by the Energy Select Sector SPDR Fund (XLE) and the SPDR S&P Oil & Gas Exploration & Production ETF (XOP), have risen 52.1% and 62.0%, respectively, from the March 23rd broader market low, and basic material stocks, as measured by the SPDR S&P Metals & Mining ETF (XME), which have risen 39.5% since the March 23rd broader market low.

Said another way, inflation sensitive and economically sensitive equities are quietly outperforming.

At the time of this publication, I was routinely mocked, much as I was in 2008 and 2009, before this happened.

How did I achieve this performance?

Simply put, it was buying undervalued equities, like General Growth Properties, in November of 2008, that almost nobody else wanted.

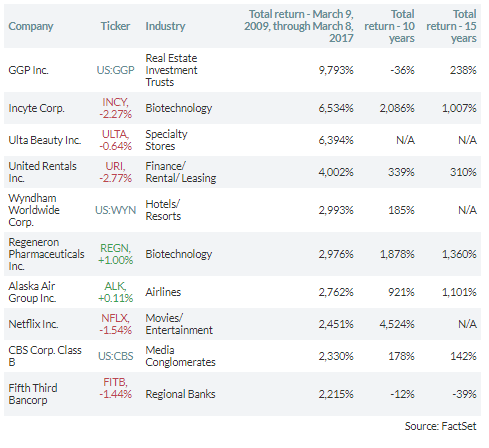

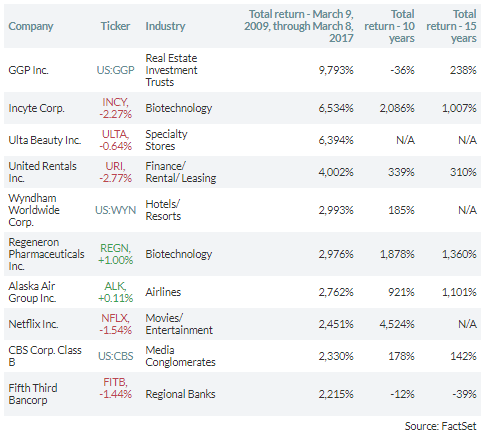

As I have said previously, these purchases, in aggregate, totaled $53,593.71, which was not a big dollar total in aggregate, however, the 120,000 shares were a nice stake in what would become the best performing S&P 500 equity in the bull market, at least through March 10th, 2017, as this CBS MarketWatch article on the bull market turning 8 years old chronicled.

In March of 2018, in the Brookfield Property Partners deal, these shares could be exchanged for $23.50 in cash.

Not a bad return at all, however, the key was to buy into the panic. That is the same thing we have done this time, and now we will see if the proverbial Main Course plays out in front of our eyes.

Best of luck to everyone. Stay healthy, safe, and happy,

Panic selling in the broader stock market may have just begun.

Under the surface, panic selling has been ongoing in selected sectors and stocks for an extended period of time.

This presents the historic opportunity.

Introduction

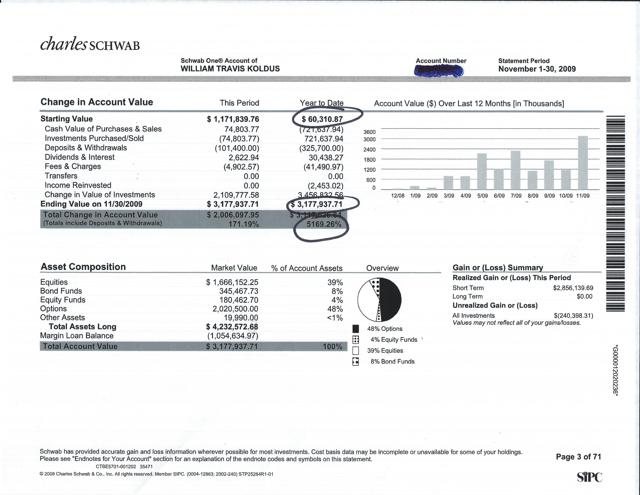

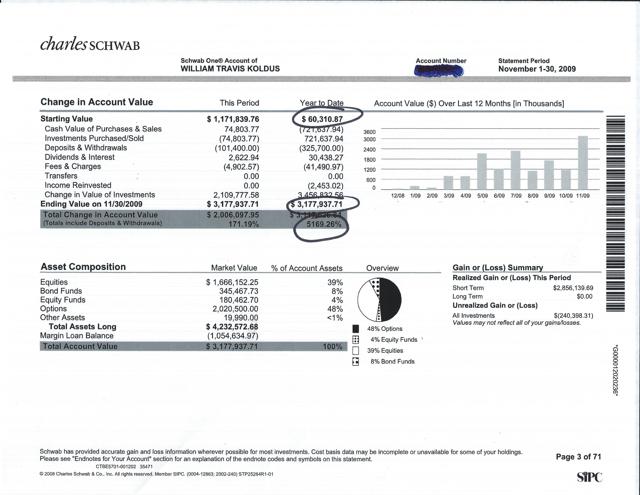

Often, I get the question of how I have achieved out-sized returns (and losses) in the past, particularly with an emphasis on what I have been able to do in my very good years, including 2016, 2003, 1999, 2000, 2008, 2010, and most notably 2009, as illustrated by the snapshot of an aggressive Portfolio that I managed personally for myself below, where I took roughly $60,000 in November of 2008 to over $3 million by November of 2009.

How did I achieve the above returns, over 5000% in a years time (which BTW I may never top, however, knowing this reality, does not stop the pursuit of good years, particularly at inflection points)?

There is a lot of complexity in the answer, including having a variant view, specifically on the broader market as measured by the S&P 500 Index (SPY), using some leverage to express this view, primarily via options, which can be very dangerous tools in inexperienced hands, and the willingness/ability to go against the grain.

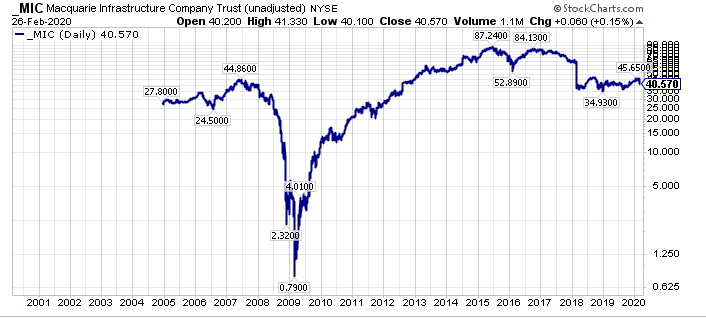

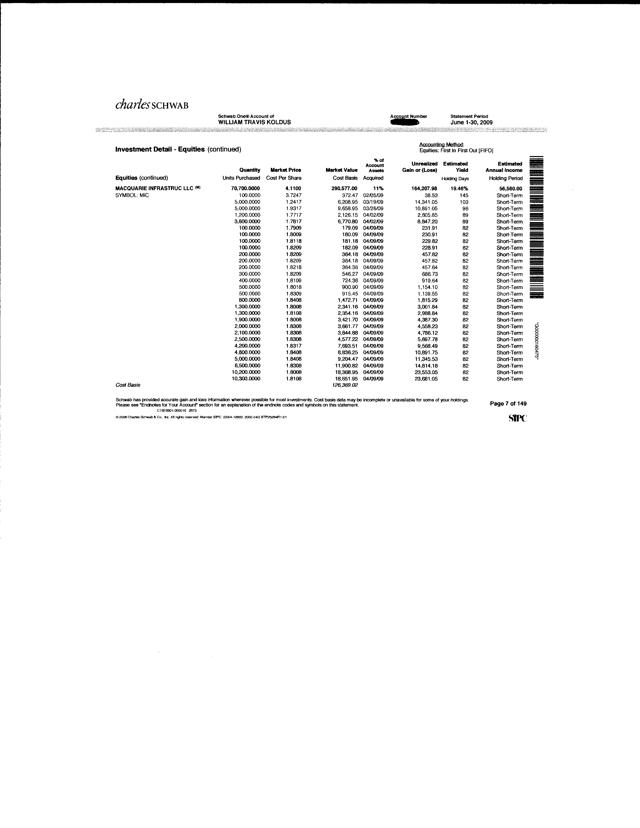

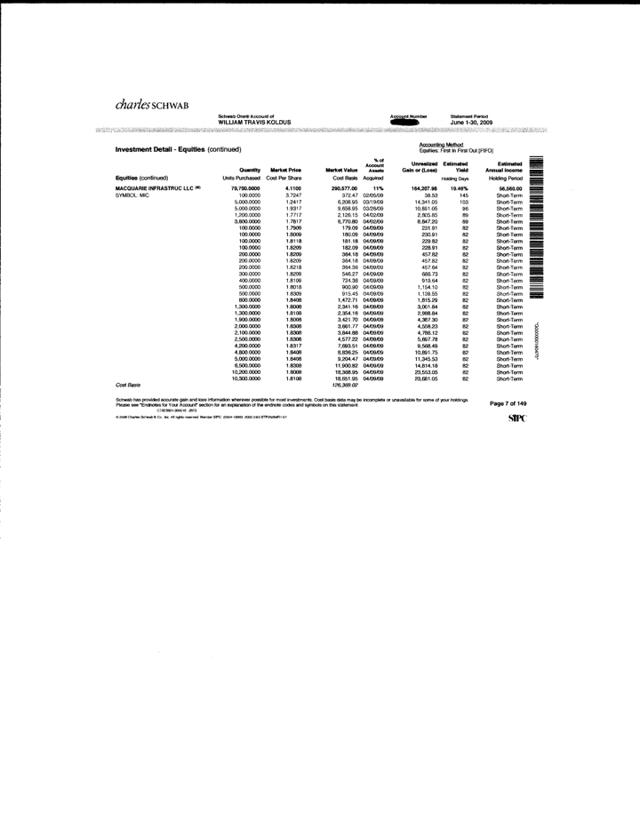

Having said this, there is also a lot of simplicity in the answer, specifically in the main underlying driver of the returns, which was buying significantly out-of-favor equities, with one example being my March 2009 and April 2009 purchases of Macquarie Infrastructure (MIC) for roughly $2 a share. Famously, MIC got down to $0.79 (before dividend adjustments…so I was down roughly 60% on even what I thought were bottom ticking purchases…think about that for a minute) and topped $80 per share, again before dividend adjustments, while also reinstating a substantial dividend, that has been roughly $1 per quarter for some time now (this dividend had been suspended in 2009 before being reinstated).

Clearly, with the benefit of hindsight, purchasing MIC at the lows was a generational investment opportunity, however, it was not easy at the time, even though I had done thousands of hours of due diligence on the company, similar to the focused due diligence effort I have done today, on out-of-favor, undervalued securities.

The key was buying into the panic selling, taking advantage of the panic, and I think we are seeing similar levels of opportunity today, just not in the places that most investors want to look.

Buying Into The Panic

In my November 2008 to November 2009 example above, I actually started buying what I felt were the most distressed, highest return potential candidate equities in 2008, in the heart of the panic. Remember, the broader equity market did not bottom until March of 2009, which is a whole other story, however, the important point is that some of the most downtrodden equities made their lows prior to the broader market making its lows.

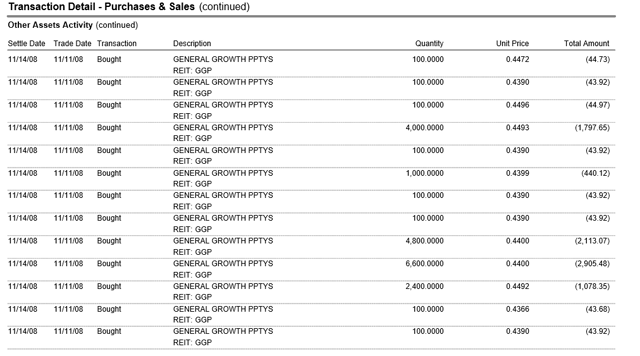

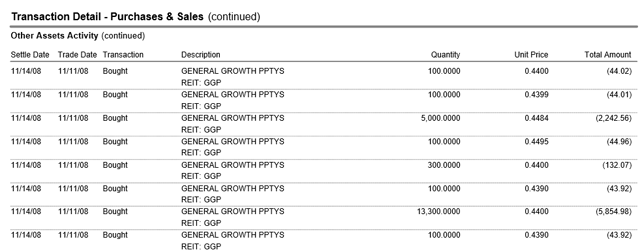

One specific example, is General Growth Properties, the former second-largest mall REIT in the U.S. behind Simon Property Group (SPG), that was eventually acquired by Brookfield Property Partners (BPY) in 2018.

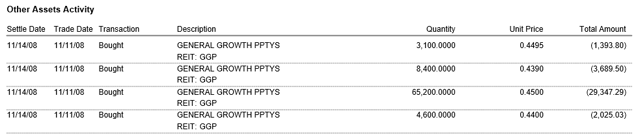

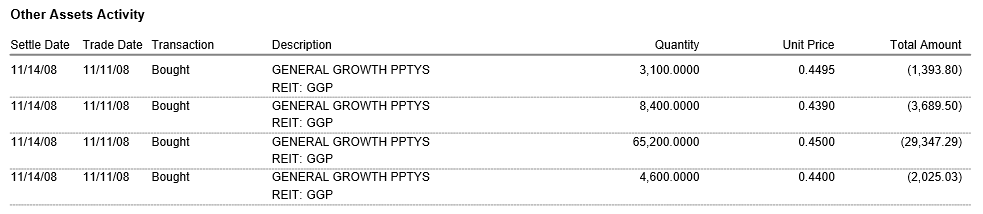

In November of 2008, I was on a due diligence trip through South Florida, meeting with hedge fund managers, and asset managers, and after a legendary night out for this generally non-party owl author (ask me for details if you want), I awoke in my Miami Beach hotel room, looking out at the ocean, and taking in the panic, eventually buying 120,000 shares of GGP on November 14th, 2018 for this specific account, as my brokerage account statement shows (if you want additional details send me a direct message).

These purchases, in aggregate, totaled $53,593.71, which was not a big dollar total in aggregate, however, the 120,000 shares were a nice stake in what would become the best performing S&P 500 equity in the bull market, at least through March 10th, 2017, as this CBS MarketWatch article on the bull market turning 8 years old chronicled.

In March of 2018, in the Brookfield Property Partners deal, these shares could be exchanged for $23.50 in cash.

Not a bad return at all, however, the key was to buy into the panic.

Where Is The Panic Today

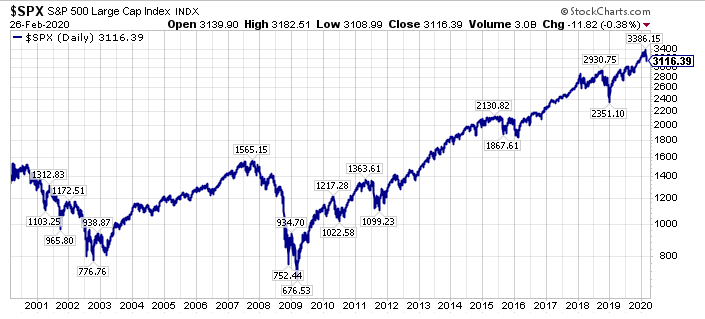

Even though the S&P 500 Index is on track to be down 7% or more this week, as I write this post, the real panic is not in the broader stock market, at least not yet.

In fact, on a long-term chart, the recent decline is just a blip.

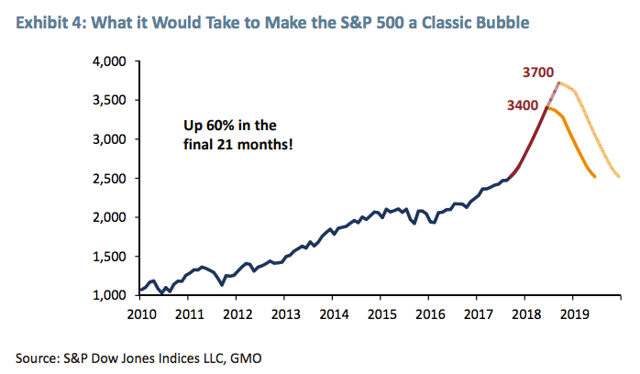

Now, we could be on our way to a broader stock market sell-off, as GMO has previously outlined earlier in 2018.

Regarding the path of the broader markets, that is yet to be determined, as we grapple with historically extended valuations, and historical monetary policy accommodation levels.

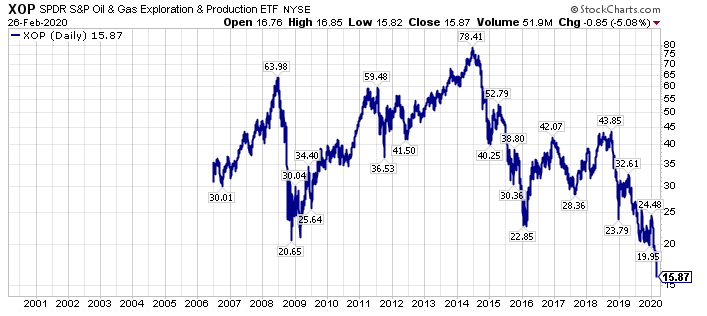

The real panic right now is in the underbelly of global economic activity, specifically in economically sensitive cyclical stocks, and more specifically, in the most loathed of all stock market sectors today, which is of course, the energy sector.

The SPDR S&P Oil & Gas Exploration & Production ETF (XOP) offers a glimpse of this panic, with XOP down 79.8% from its 2014 high, and down 63.8% from its 2018 high.

Thus, with the broader U.S. stock market, as measured by SPY, only down roughly 8% from its recent highs, the compare & contrast should be eye opening for most investors.

Building on the narrative, with our deep research dives, we feel there are a number of out-of-favor equities that are down even greater in percentage terms, which offer even greater relative and absolute opportunity.

Importantly, similar to several of the downtrodden equities I purchased in late 2008, and early 2009, including General Growth Properties, and Genworth Financial (GNW), which was also bought well below $1 in November of 2008 before shares rebounded above $18 by early 2010, the most out-of-favor, undervalued equities right now, will probably bottom ahead of the bottom in the broader equity market.

Panic Selling Is Yielding Opportunity

It is no secret that I am targeting what I believe are the most undervalued securities, with the goal of creating a generational wealth opportunity. These securities are generally loathed, unloved, and scorned right now, and many of these equities would make your stomach turn looking at long-term charts, part of the reason there is so much opportunity.

While the best opportunities are generally in smaller capitalization names, there is opportunity in large-caps, including in energy stalwarts like Exxon Mobil (XOM), Occidental Petroleum (OXY), and Schlumberger (SLB), all of which offer attractive yield-oriented income opportunity.

These three securities are part of a “Stuck On Yield” Model Portfolio, which is a $100,000 portfolio, that I created on Friday, February 21st, for a family member.

This Portfolio is yielding over 14% right now, and I have done deep-dive due diligence on all its member components, a majority of which are from the target rich energy sector.

Members of The Contrarian can see this Model Portfolio here, and I have sent out emails of this Portfolio to members of my research services, and I will be making it available this week for all my research members.

Closing Thoughts – Be Ready To Buy Now

Nobody, including me, really knows where the stock, bond, and commodity markets are headed right now with certainty. All we have is probabilities, and ultimately, our valuation analysis. The latter is crucially important, as buying the most undervalued assets, ultimately leads to the strongest returns, so long as you can ascertain the underlying asset quality, and survivability of the corporate entity.

On this note, I am going to make mistakes, so the key is getting a handful of these right, as the gains from the survivors will more than make up for any losses, at least that is my past experience at previous inflection points. Ultimately, valuation matters, and starting valuations levels matter too. Adding to the narrative, with everyone wanting to own quality today, there are many “Have Not” securities that are historically undervalued.

Conversely, a high valuation is a bad starting point, and buying overvalued assets, which certainly describes the S&P 500 Index, which trades at greater EV/EBITDA, Price/Book, and Price/Sales multiples that it did at its peak valuation levels in late 1999/early 2000, is a recipe to achieve poor returns going forward. Adding salt to the wound, the bond market, which offers meager sovereign yields, is also set-up for poor future returns over the longer-term, as historically over 90% of bond returns are correlated with starting yields.

In summary, buy what is cheap, andbuy into the panic, as the cheapest valuation equities with the best future return prospects will often rebound ahead of a bottom in the broader equity market.

Specific to my research services, I am offering a 20% discount to membership (I am extending this through March) to “The Contrarian” (past members can also direct message me for a special rate), the lowest price point since the founding members price, where we have a live documented history dating back to late 2015..

Additionally, I am offering a limited time 50% discount for the first 5 new members (I expect these slots, some of which I view as a stepping stone to “The Contrarian”, to fill up fast as they have done previously) to a host of research options, including a lower price point. If you subscribe to a premium option (I have had one concierge slot open up after a gentleman I was speaking to last evening held off on taking this slot), I will set-aside time for a personal phone call to get up to speed. To get these offers, go here, and enter coupon code “opportunity” without the quotes.

Reach out with any questions via direct message (I enjoy the dialogue at market inflection points).

Via my research services, or another avenue, please do your due diligence, and take advantage of what I believe is a historic inflection point, which I believe will supersede 2000-2002 in the growth-to-value rotation.

Disclosure: I am/we are long MIC, OXY, SLB, xom and short spy in a long/short portfolio.

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.

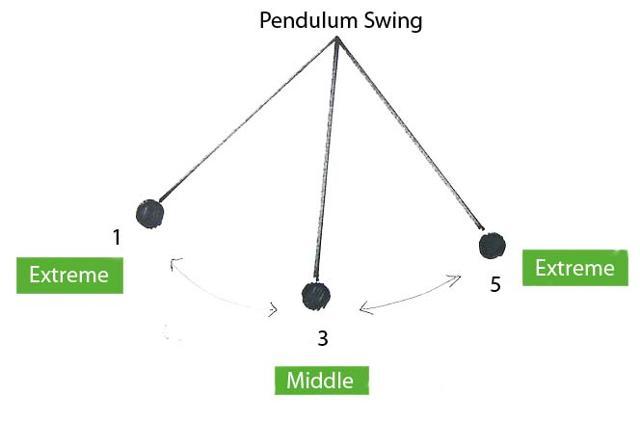

Passive index investing has dominated fund flows for a long time, accelerating over the past decade.

Once vaunted value investors have been left behind, as have a whole group of out-of-favor, forgotten equities.

The pendulum has swung too far to one extreme, and appears to be starting its move in the other direction, offering historic opportunity for forgotten equities.

I grew up, and have spent almost all my life in the great state of Indiana, though I have traveled across the United States, and a little bit of the world (I want to travel more) in my career, and for pleasure.

Growing up in Northwest Indiana, which was really an extended connection to Chicago, referred affectionately to those from this area as “The Region” (I actually used to tell people that it was really like growing up on the South Side of Chicago, but true South Siders take offense to that), I went to college for undergrad studies at Ball State, in Muncie, Indiana, then moved to various suburbs around Indianapolis, working first in a suburb, then in downtown Indianapolis, then in a suburb again, before starting my own boutique investment research firm.

More recently, my life, which is a story on its own accord, for a book that would make interesting, perhaps even good reading, even for those not financially inclined, and my career to an extent, has taken me to various small towns across Indiana (and some of the bigger cities too…which outside of Indianapolis are really pretty small on a national scale, with the possible exception of Ft. Wayne), and even though I love geography, and enjoy driving, it is amazing to me the number of different small towns that I was unaware of, and stories behind them, which I am sure is true in a number of states, however, I have not traveled them nearly as much.

Many of these small towns, dotted in-between the never ending corn and soybean fields, which can be a beautiful backdrop driving, especially in the changing seasons, are forgotten by those in the bigger cities in Indiana, which really, again, there are not many of, let alone on a national scale. Summarizing, I have spent virtually my whole life in Indiana, and I come across new towns and places on a regular occasion, with their own interesting backstory and history.

Building on the narrative, even though Indiana is home to a number of Fortune 500 companies, including Eli Lilly (LLY), Cummins (CMI), Steel Dynamics (STLD), Zimmer Biomet Holdings (ZBH), Berry Global Group (BERY), which honestly I had not heard of before today and I have spent my past 25 years actively research and investing, and Simon Property Group (SPG), and a number of S&P 500 Index (SPY) companies have significant operations located in Indiana, which is a list too big to show in its entirety, including somewhat surprisingly Salesforce.com (CRM), on this note Indianapolis is also a finalist for Amazon’s (AMZN) second headquarters search, and a number of global industry leading companies have significant operations in Indiana including ArcelorMittal (MT), and Roche Holding Ltd (OTCQX:RHHBY), (OTCQX:RHHBF), Indiana is an overlooked state, in my opinion, on a national profile.

Sure, we in Indiana have globally recognized institutions with significant fan followings, including Notre Dame football in South Bend, Indiana basketball in Bloomington (though they have been in a down cycle, they are still a sleeping giant with a level of national success that only a few other programs can match), heck even the much maligned NCAA headquarters is located in Indianapolis.

The college programs and towns in Indiana are terrific from Purdue in West Lafayette, to Indiana University in Bloomington, to Notre Dame in South Bend, to Butler and IUPUI, both in Indianapolis, to Indiana State in Terre Haute, and Rose-Hulman Institute of Technology in Terre Haute (Rose-Hulman, which I go to on a regular basis, and Purdue are two of the finest engineering schools in the country), and right on down through the smaller colleges such as the University of Indianapolis, DePauw University in Greencastle, Indiana, (the only time I ever ran of gas driving, which occurred recently, was near Greencastle, where a nice man, resembling a younger version of my deceased for seven year father, and having his same first name, picked me up and helped me on my way), and Wabash College in Crawfordsville, Indiana.

Speaking of my deceased father, who I wrote about more here, we used to travel the state together for a couple reasons. First, he was an athletic director, and coached a bunch of sports, so by default their was regional and statewide traveling. Second, we both loved Indiana high school basketball, particularly before the winner-take-all tournament was changed, and third, my dad had a love for track-and-field, which he coached at the high school level too, and followed with interest around the state.

Interestingly, the professional sports teams in Indiana, including the Indiana Pacers, which I had tickets too for some time, including when they collided with the Miami Heat team four consecutive finals team, led by LeBron James and Dwyane Wade, and the Indianapolis Colts, probably have less state and national followings that Notre Dame football or Indiana basketball.

In summary, Indiana offers a rich fabric of nationally recognized colleges, and internationally recognized companies, yet while parts of Indiana thrive, there has certainly been a number of small towns, companies, and industries that have been left behind.

On this note, both of my parents were raised in Gary, Indiana, which was once, long ago, one of the most thriving cities in America, yet today, the southern Lake Michigan industrial coast line, from East Chicago to Hammond to Gary, is a shell of its former glory.

Jobs were cut, and industrial production centers centered in the Midwestern United States lost their place in the global supply chains.

Even though the fortunes of many of these companies have been revitalized since commodity prices bottomed early in 2016 (alongside a bottom in global growth), followed by a bottom in sovereign bond yields (with a corresponding top in bond prices), the broader U.S. equity market, which has been dominated by a handful of winning companies, and winning sectors since the current bull market began in March of 2009, has overlooked a small, but significant group of companies, overrun by the passive flow driven rally.

Additionally, many stock markets outside the United States, and associated targeted companies have been left behind too, as global capital fund flows have been recycled to the United States this past decade, driving up the U.S. Dollar Index, and combining with domestic fund flows to passive and ETF passive strategies, to narrow the global equity bull market, led by U.S. equities, to a significantly smaller group of winning companies that one would expect, given the magnitude of the equity rally.

Collectively, the left behind companies and their associated equities, both domestically, and internationally, where there is a greater number of these mis-priced companies, in my opinion, are theforgotten companies.

This is a term, the forgotten companies, that I am going to use over-and-over in the next several weeks and months, to describe the group of undervalued companies that offer rare opportunity, in their equity prices.

For a first-look at the forgotten companies that I will be covering in-depth, and have been covering in-depth, please consider joining The Contrarian, which is my premium research service platform on Seeking Alpha.

I am biased, of course, but I think we have the best group of investors and traders anywhere, seasoned by nearly three years of experience together, positive and negative, and commentary for some members, with many members actively contributing their unique perspectives to a robust Live Chat discussion on a daily basis, particularly when volatility surfaces.

Right now, we have an open free trial at The Contrarian, so if you have ever had an interest in test driving our group, now is a good time.

From my perspective, as I said in my blog posts the past week, it would be worth taking a look, simply to view the Live Chat dialogue.

The price point of The Contrarian is a little steep, coming in as one of the more expensive services in SA’s Marketplace.

Over the years, I have had quite a few requests for a lower-priced, more streamlined research product, and over the last several months, I have slowly put together a more traditional research newsletter.

Ultimately, I think we are now at a major inflection point in the financial markets, which has been ongoing in slow motion for three years, but which could suddenly accelerate. Being different, being contrarian, has been extremely painful for a long time now, however, resilience and persistence, two necessary qualities for success in contrarian investing, in my opinion, are leading to what I believe is an upcoming golden age for active investors.

Disclosure: I am/we are long CLF, MT, X, and short SPY as a market hedge.

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.

Spanish football giant Barcelona has an famous youth academy, called La Masia de Can Planes.

This academy is widely regarded as the best in the world.

Through training hundreds of players, they have found that the number one predictor of success is resilience. I believe the same thing is true for investing and speculating.

(Picture above drawn by my daughter after she was put in timeout)

About a month ago, I was listening to a podcast with Bill Simmons and Steve Nash, and something they were discussing caught my attention.

Specifically, around the 28 minute mark (I would encourage everyone to listen because it really is a good conversation), Steve Nash was talking about the predictors of success in player development, and he referenced the youth academy of soccer giant Barcelona, known as La Masia de Can Planes, often shortened to La Masia.

“La Masia de Can Planes, usually shortened to La Masia (Catalan pronunciation: [lə məˈzi.ə]; English: “The Farmhouse”),[1] is often used to generically describe the Barcelona youth academy. This academy holds more than 300 young players, and has been praised since 2002 as the best in the world, being a significant factor in FC Barcelona’s European success.”

Nash said that La Masia had found, in its training of the most world class soccer players by any youth academy, that the number one predictor of success was resilience.

Think about that for a second, for developing youth soccer players, the number one predictor of success in the youth academy was not height, strength, speed, coordination, or athleticism, but rather it was resilience.

During the conversation, Nash said that resilience is not really taught, which should be addressed differently.

Nash and Simmons went back and forth ib whether was resilience was something you have inherently, or if it could be trained, or taught.

This observation about the importance of resilience got me thinking about investing, and speculating, and from my personal experiences, my biggest successes usually have occurred after periods of prolonged pain & suffering, or said another way, trials and tribulations. In short, my biggest triumphs investing and speculating almost always required resilience.

Looking at it from another perspective, sometimes investing, or speculating, (or even life) goes against you, maybe even in a big way, and when this happens, it is crucial, in my opinion that you have resilience too.

Not giving up, keeping at something, this persistence & resilience is not common if something not going a persons way. Often times, it can lead to success.

One caveat with investing and speculating though, and I suppose this is true in life too, is that I have learned persistence and resilience, or not giving up in the wrong situation, can lead to less than ideal outcome or even catastrophic losses.

So, I suppose the lesson is to be resilient at all times, through successes and failures, and be persistent/resilient if you have reason to believe that failures will eventually pay dividends.

In summary, do not discount the importance of resilience in investing and speculating, or in life,

WTK

P.S. The attached picture above is drawn by one of my daughter’s, composed after she was put in “timeout” that she felt was undeserved, and thus she wrote, “Life Ain’t Fair”. That is certainly true, and I would add the markets are not fair either, however, it is the job of a successful investor or speculator to have resilience, and take advantage of the price dislocations.

(This article was published on August 28, 2018, and is being re-published on October 28th, 2018 to add to the archives.)

This was an actual conversation today.

Seeing the world through the eyes of a 6-year old.

Did Toys “R” Us have to liquidate?

Today, I picked up my youngest daughter from school. The following was the actual conversation to the best of my memory.

(WTK): I am here to pick you up.

(Daughter): Where is mommy?

(WTK): She is teaching middle school today and is with your sister’s class.

(Daughter): Ask Siri on your Apple (AAPL) phone where I can buy L.O.L. dolls?

(WTK): Why would I do that? They are like $30 or something like that. The only person L.O.L’ing is the people who are selling these.

(Daughter): What? Never-mind. You can buy them at Target (TGT), Wal-Mart (WMT), and you used to be able to buy them at Toys “R” Us.

(Daughter): I have one question. Why did they close down Toys “R” Us?

(WTK): Do you really want to know?

(Daughter): Yes.

(WTK): Toys “R” Us had too much debt from when private equity players Bain Capital and KKR (KKR) teamed with Vornado Realty Trust (VNO) for a leveraged buyout. They had to pay too much interest from this debt, and with competition from Amazon (AMZN), Target, and Wal-Mart, it was too much. Also, believe it or not, five hedge funds who held their debt, including Oaktree (OAK), who you care nothing about, made the decision to close down the Toys “R” Us stores, rather than keep them operating.

(Daughter): Wait…wait a minute. So they did not close down the stores because people were not buying toys there?

(WTK): That was part of it, but mostly it was the interest on the too big of pile of debt.

(Daughter): That is so frustrating. Now I can’t buy L.O.L. dolls at Toys “R” Us anymore. Life is so unfair.

(WTK): Unfair? I will tell you about unfair. Did I ever tell you I got the big picture right for coal, meaning a historic turnaround in coal prices, yet distressed debt buyers got all the benefit.

(Daughter): I do not want to hear about that anymore.

(WTK): Anymore?

(Daughter): I just want to talk about Toys “R” Us. It does not make sense.

(WTK): I know.

P.S. When I was a young kid, all I wanted to do was have enough money to buy whatever I wanted at Toys “R” Us. I guess somethings never change.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.

(Travis’s Note: This article was originally published on April 24th, 2018, and it is being republished on October 28th, 2018, to add to the archives.)

For over nine years, the current bull marked has surprised investors and speculators, including me, with amazing twists and turns.

Personally, I benefited at the previous two major inflection points, (2000 & 2008), including making money in 2008, and making a small fortune in 2009 on the long side.

Lessons learned in 2008 & 2009, and during the prior 15 years actually created value biases in my investing style that impaired results tremendously in the current bull market.

The pain culminated in a horrific 2017 for me personally, which ironically had followed a historic rebound and reversal in 2016.

Almost everybody’s an expert today, with biases in their own successes over the current bull market, or over the past 20 years, but that market environment is rapidly coming to an end.

Few investors and speculators have had the highs, which included making money personally in 2008 followed by huge success on the long side in 2009, or the significant lows, including losing large sums of money personally and for individuals that I was/am very close to (there is nothing more torturous than believing in something through thousands of hours of research, sometimes tens of thousands of hours, and the market proving you wrong, and failing people who are close to you) that I have experienced in the financial markets.

I am over 40 now, and I have been investing for nearly 30 years, starting when I had a paper route at 9. This has accumulated to a fairly large pool of experience.

However, that only tells half the story. Financial markets, and market history have been a large part of my life beyond simply the years accumulated, as they have been both a passion and a hobby.

From the age of 12 to 15, I consumed every financial book I could find (really ever since that time frame I have been a voracious reader – this is my favorite financial book), and I began more actively investing and speculating in my early years of high school.

One of my favorite books from this time frame was Martin Zweig’s Winning On Wall Street, which was published in 1986. During my formative years, I also read the Wall Street Journal, Barron’s, and Investor’s Business Daily, which was founded my William O’Neil in 1984.

During college, I switched from a career in teaching, following in the footsteps of my deceased father, into a career in Finance, after I turned a $3,000 student loan into over $300,000. I spent every free minute or hour studying the markets, and I figured that I should make a career out of the profession, since it was something I had a unique passion for and where work felt more like a hobby.

Academically, I graduated Summa cum Laude, as the Top Finance student in my class, while working all kinds of jobs from resident assistant, to waiter, to hotel front desk worker, to an internship under a renowned value investor at an insurance company.

From there, I have held many licenses, and accreditation’s, including achieving the CFA Charter in 2006, and the CAIA Charter shortly thereafter.

Additionally, I have spent almost my whole adult professional career in the financial markets, working for Charles Schwab, then performing research as an investment analyst for an RIA, then working for one of the largest RIA’s in the country as a senior investment analyst.

Along this journey, I started a boutique invested firm with my own capital in 2009, I have helped to host investment conferences, and I have consulted for some renowned hedge funds.

Then, late in 2015, I founded “The Contrarian“, because I believed we were near another major inflection point.

In 2016, I was spectacularly right with this forecast.

Then, shortly thereafter, I was spectacularly wrong in 2017, where a huge curve ball was thrown by the markets, which has tested my spirit, persistence, and drive like few challenges in my life.

The financial markets are notoriously humbling, as life is, and 2017 humbled me mercifully, as investors went back into the same trades that excelled from early 2011 to early 2016, even though we had major secular turning points in 2016, including bottoms in commodity prices, including in oil, in interest rates, and a top in the U.S. Dollar.

In summary, the gravitational pull of the bull market was so strong, and so distracting, that it lulled everyone into thinking that nothing had changed in 2016, even though everything had changed.

Even more alarming, the increasingly rare events became prized as commonplace in the financial markets.

How does this happen? The pied piper of the Fed and global central banks have certainly not helped, yet it is just the human condition, where we have all become accustomed to excessive speculation and extraordinary intervention in the financial markets.

Following the most improbable losses of my investing career in 2017, I believe there are extraordinary opportunities in today’s financial markets on both the long and short side.

Thus, while most traditional investors could probably “Take A Ten Year Vacation“, and check in quarterly or annually to see if there are better opportunities, and most likely, come back to better prices a decade from now in the broader U.S. stock and bond markets, the landscape for contrarian value investors is unusually opportunistic, as most trades are extremely one-sided today, and when the pendulum swings the other way, it is going to be something we are writing about like we write about 1999-2002 and 2007-2009.

In closing, I have gone on several tangents, however, the main purpose of this blog entry is to highlight the opportunity, highlight the risks, and just reflect a little bit in a public forum where a dialogue can ensue.

When the extraordinary happens over and over, it becomes routine in a sense. Thus, for investors who have lived through the late 1990’s and early 2000’s, or those who survived and thrived from 2007-2009, today’s extremes seem commonplace, yet today’s extremes are even more extreme than those historic extremes.

If you take away anything reading this, be aware of the market extremes, be aware of your own biases, my own have been exposed and beaten down, and be aware of the historic risk, and the historic opportunity.

WTK

Disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.

(Travis’s Note: This article was originally published on January 29th, 2017, and it documented a journey from out-of-favor to in-favor, that I anticipate will repeat over additional cycles.)

“Time is the coin of your life. It is the only coin you have, and only you can determine how it will be spent. Be careful lest you let other people spend it for you.”

Carl Sandburg

“Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria”

Sir John Templeton

“Life and investing are long ballgames.”

Julian Robertson

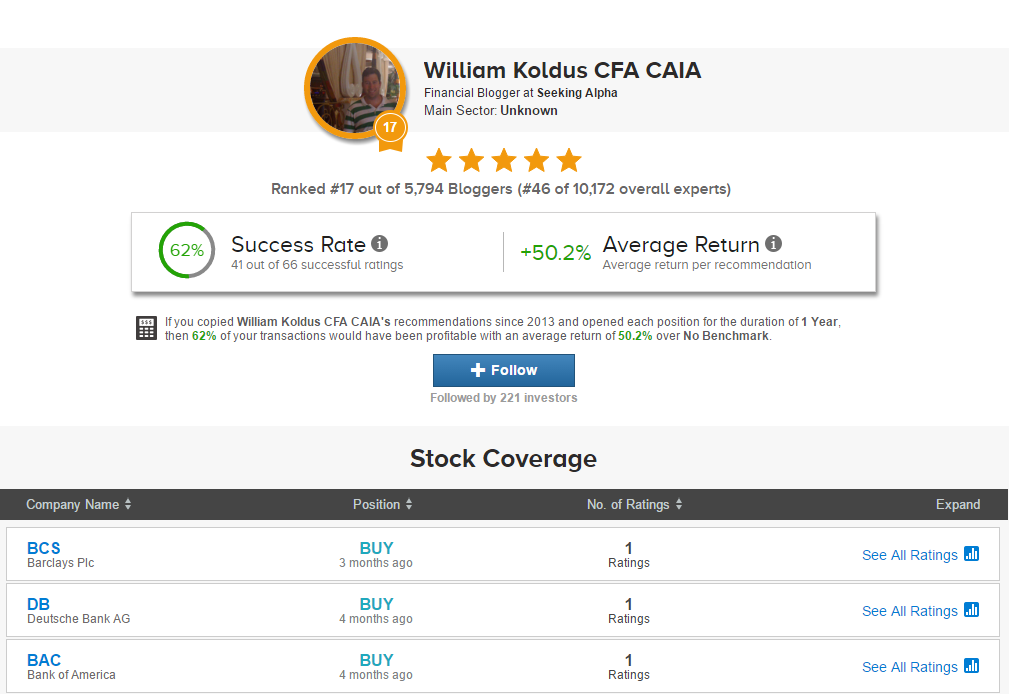

One year ago, on January 29 th, 2016, I looked at my TipRanks.com profile, and I was the 4,380th ranked blogger out of 4,802 bloggers. Additionally, I was the 7,829th ranked “expert” out of 8,501 ranked “experts”.

Needless to say, my public profile as a research analyst, nearly 20 years into my career, was less than acclaimed. Additionally, I had my fair share of detractors on Seeking Alpha, and outside Seeking Alpha, who did their best to remind me of just how incompetent I was in my research analysis.

Fast forward a year later, and the narrative has changed. Today, January 29th, 2017, I am the 17th ranked blogger out of 5,794 bloggers, and I am the 46th ranked “expert” out of 10,172 overall “experts”.

While I made some big mistakes, and learned some invaluable lessons along the way that I will never forget (I have the scars to prove this) in this constantly learning business, persistence, stubbornness, and hard work ultimately paid some dividends.

The lesson for all investors is that you have to be careful judging an analyst, or even yourself, good or bad, because the view could change as the perceptions and realities of the market change. Additionally, another lesson is that it is difficult to take a variant view, as the markets have a way of punishing the alternative view for a long period of time.

In “The Contrarian“, the premium research service I founded on Seeking Alpha on December 7th, 2015, we actively challenge the status quo in search of out-of-favor investments that have inherent potential opportunity. Additionally, we challenge each other to become better investors, speculators, and traders.

While I could go on and on about the merits of the service (admittedly I have a biased view), and how much I enjoy writing and participating in it, member reviews provide another perspective, and I wanted to share this information once again, as there are now 21 reviews, all “Five Stars” at the current juncture.

Without further ado, here is a link to all the reviews of The Contrarian. Please check them out for yourself. Thank you to all members of “The Contrarian” for creating a unique community that I am privileged to participate in every day. Also, thank you for taking the time to read this article. If you are interested in joining our community, which I think is timely today, follow the prompts, and reach out with any questions,

Travis

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.

(Travis’s Note: This article was originally posted on July 8th, 2015, however, the trades described were made late in 2008, and early in 2009. One learning lesson from this experience, is that if you buy a deep value equity, and you are right, and the situation resolves bullish, your price targets in the depths may be way too conservative, and it is probably better to hold on to this uncovered treasure longer than you think at the time of purchase).

Purchasing Macquarie Infrastructure (MIC) in the first half of 2009 has been the best equity trade of my career thus far:

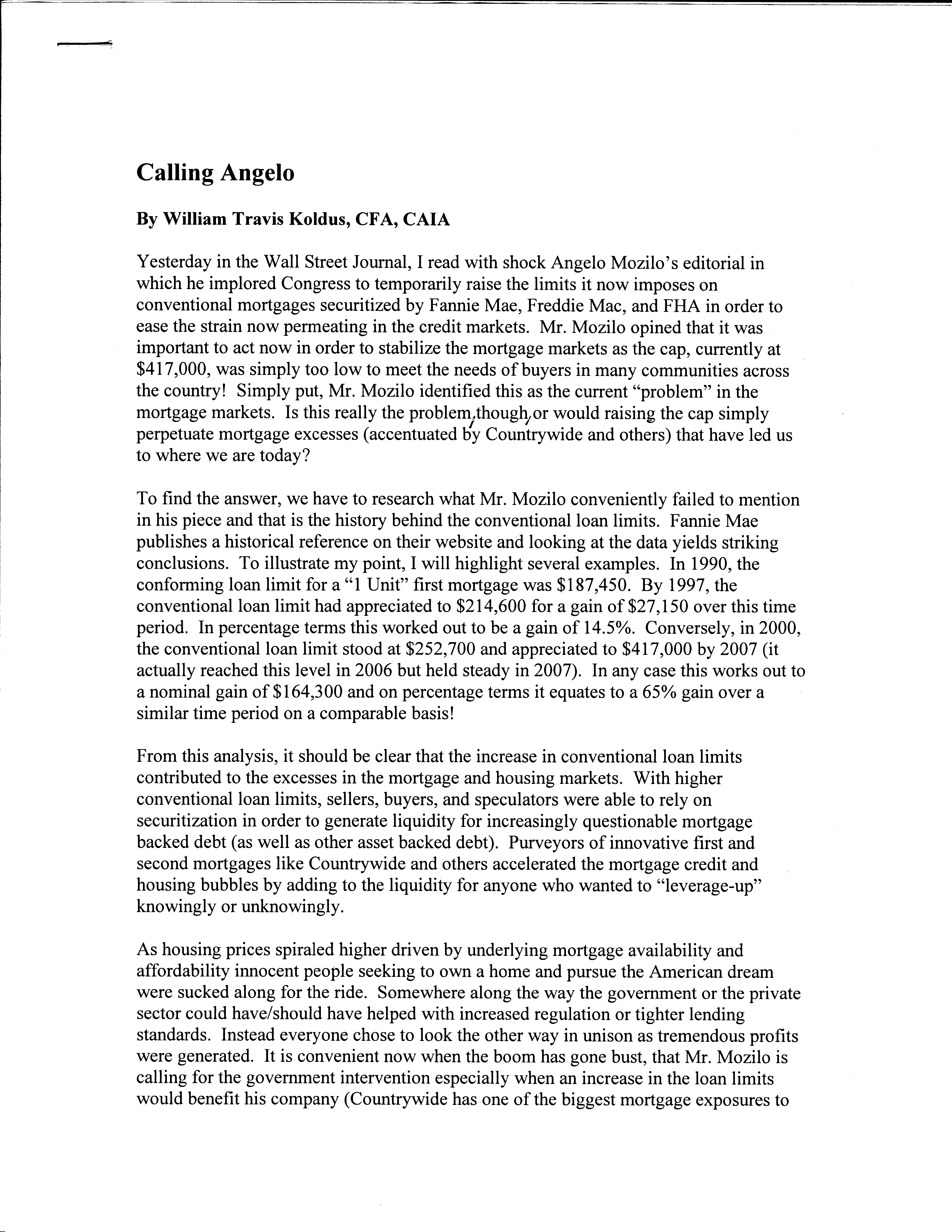

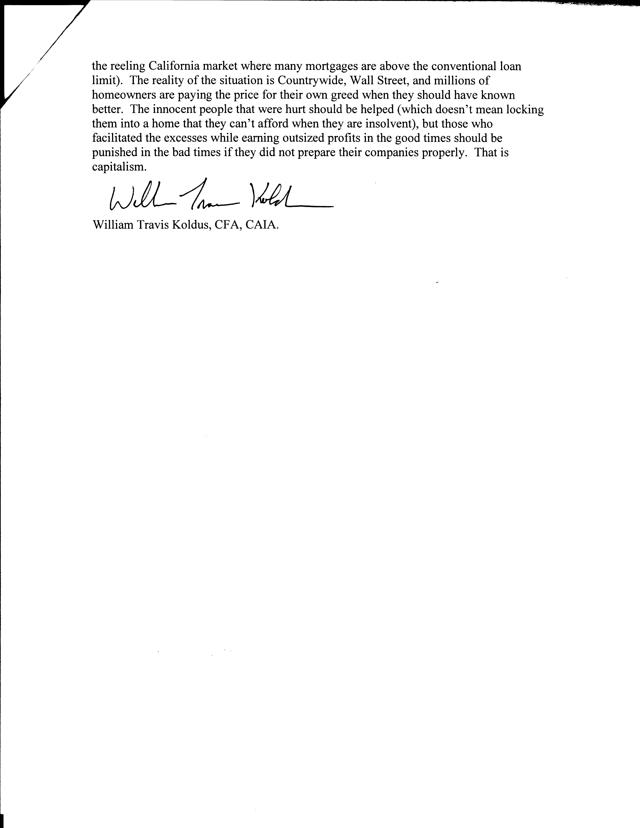

(Travis’s Note: I posted this article originally on May 22nd, 2015, however, the letter authored in the article was submitted on December 6th, 2007).

This is a flashback to a editorial, which I found this morning going through some research and then I scanned, I submitted to the Wall Street Journal on December 6, 2007. It was written in response to an editorial by Angelo R Mozilo, titled “Calling Fannie and Freddie”, which was published in the WSJ on December, 5, 2007, in which the former CEO of Countrywide implored Congress to temporarily raise the limits it imposed on Fannie Mae, Freddie Mac, and FHA mortgages by 50% in order to stabilize the mortgage markets. Here is my response:

It has been a long, difficult stretch, yet there is light at the end of the tunnel.

Prepare accordingly for the opportunity.

(WTK’s Note: This picture shows how I want to feel after downtrodden, out-of-favor value equities reclaim their rightful mantle of the stock’s markets best performers…actually poor Andy suffered long after this scene…so really I want to feel how he felt upon reaching Zihuatanejo..for more of my take on the Shawshank Redemption and how it applies to investing…read this post).

When I was sixteen, which is now twenty-five years ago, I bought a brand new GMC Sonoma blue pick-up truck, which I drove right until it died on me in an apartment parking lot roughly a decade later.

The blue GMC pick-up truck was partially funded from my paper route, which I had since the age of 9, and partially funded through ongoing work during high school, including as a dishwasher, cook at a restaurant (Schoops in NW Indiana…I could grill a hamburger with the flattened edges to perfection), and as a jack-of-all trades at St. Anthony’s Hospital, with much of my time as a stock boy.

Not that kind of stock boy, but rather actually stocking shelves, though I was already knee-deep in the stock market, actively trading at that time (without the technology comforts, or access to the markets, of today…perhaps that was a good thing).

One night when I was 16, after a long shift cooking, and closing at the restaurant, I was driving home around midnight, on an almost empty four-lane road, and I looked down briefly to adjust the radio.

Before I could look up, a car had veered in front of me, taking a sharp angle to a convenience store, that I had not anticipated.

Boom…my new blue GMC Sonoma pick-up truck rear-ends the car.

Thankfully, nobody is seriously injured.

It is my fault.

I have insurance, but what a night.

To my credit, I took responsibility. The car was fixed, lessons were learned, though I did hit a mailbox driving with my friend Marc Vassallo to work out later that summer, which was the last car accident that I had, hopefully I do not jinx myself with my remembrance.

Note to self. Be careful with oldest children (daughters) as they get close to driving age. They are too close already. Some in our family think they should not drive until 18 or 19, however, there is merit in diving in and learning, though perhaps not in a new car. They need to take risk driving to learn, to be independent, at least that is my view.

Similar to my accident when I was 16, the last several years, really a long stretch since 2012, with the notable exception of 2016, have been very difficult for my investing style, coming out of nowhere after my most successful stretch trading and investing, as value and concentrated investing approaches have been out-of-favor, and trend following, and passive investment strategies have been dominant in their performance.

Looking back, I have to take responsibility for the wrecks I have caused, meaning investing mistakes, and believe me, these hit home, as I have invested millions and millions of my own capital into what I believe are the best equity return candidates.

Eating my own cooking is the only way I know. It has worked for me before to a degree I never would have imagined, and it has failed me too, even when I was sure of something that ended up being right, but I was still wrong.

That is the cruel irony of markets, and of life too I suppose.

Additionally, I am stubborn to a fault, loyal to a fault, and competitive to a fault, while having the drive and ambition to research something for years if need be, all ingredients for big successes and big failures.

One lesson I have learned in the stock market, after 25 plus years speculating, and investing, is that you have to ask, “what may go wrong?“, even in seemingly the best situation.

Opposite, and not natural when thinking about the aforementioned question above, but a necessary ingredient too, is that investors and speculators must keep in mind “what could go right“.

Looking back on this note, my biggest mistakes in Dollar terms, has been selling something too early, after building a big position, typically in a value equity, and initially thinking I was right, and then taking profits too early.

Hubris and a need to do something are enemies in the stock market. Personally, every time my ego has ballooned, something happens to let out the air.

Patience, and acting when presented with an opportunity, are allies in the stock market.

Most importantly, though, in my opinion, is resilience, and the tenacity, and persistence to stick with an idea.

What is the point of my late night reminiscing and rambling?

It boils down to a couple things. We are all going to make mistakes investing and speculating (and in life too). Sometimes these are big mistakes. When this happens, we have to take responsibility, learn from them, and then, and this is key, not be afraid to take risk.

What is risk anyway right now?

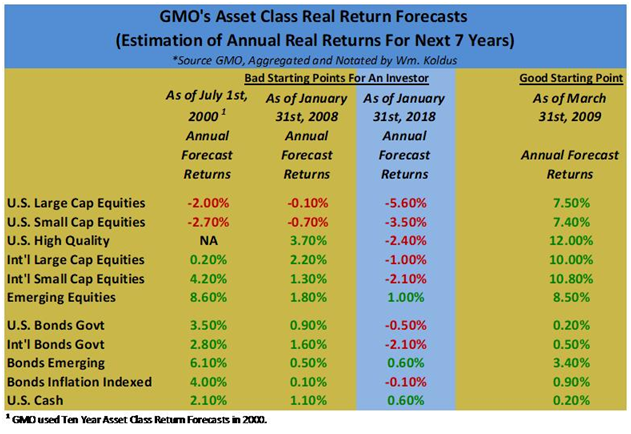

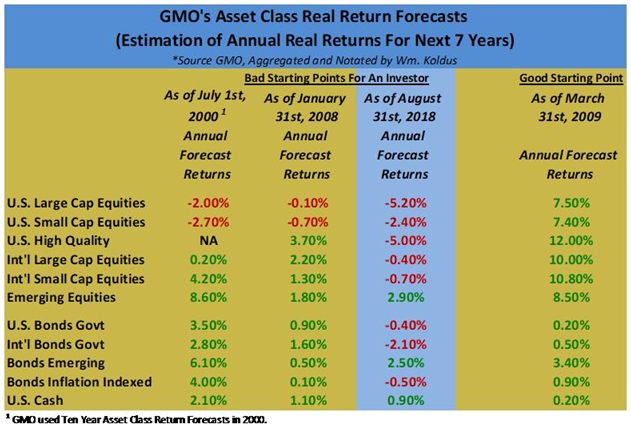

Is somebody fully invested in the stock market very risky? I would say so, given my views on market valuations, which are echoed in this long running table that I have put together that I get laughed at now for posting.

Looking at the table above, the broad U.S. equity market looks historically risky to me, with the caveat that I would have said this, using the same information, for a long time now.

So to me, U.S. equities are historically risky, with strangely many very cheap bargains, however, another person may say someone all in cash is risky.

This question of risk is all in the eye of the beholder, however, I would say after nearly a decade of the “winner’s” winning, there may be more risk in these winning equities that investors, speculators, and long-time holder imagine, and alternatively, there may be a good risk/return reward ratio (say that five times fast) in many of the out-of-favor, downtrodden equities that have generally not participated in the bull market the last decade.

Ironically, many investors would not touch these equities today, and really, who could blame them.

You would have to have the patience of Andy Dufresne, the famous flawed, resilient protagonist in Shawshank Redemption to be interested in many of these downtrodden, out-of-favor equities.

“Not participated”, by the way, is a kind term, as many out-of-favor equities, even some household names, have been crushed, far out of sight of the shiny, roughly decade long bull market in the S&P 500 Index (SPY).

The discussion of where to invest, what is risky, and what is historic opportunity, is a lively topic at The Contrarian, which is my premium research service platform on Seeking Alpha.

I am biased, of course, but I think we have the best group of investors and traders anywhere, seasoned by nearly three years of commentary for some members, with many members actively contributing their unique perspectives to a robust Live Chat discussion on a daily basis, particularly when volatility surfaces.

Right now, we have an open free trial at The Contrarian, so if you have ever had an interest in test driving our group, now is a good time.

From my perspective, as I said in my blog post yesterday, it would be worth taking a look, simply to view the Live Chat dialogue.

The price point of The Contrarian is a little steep, coming in as one of the more expensive services in SA’s Marketplace.

Over the years, I have had quite a few requests for a lower-priced, more streamlined research product, and over the last several months, I have slowly put together a more traditional research newsletter.

To celebrate this official launch, which includes a deep-dive research report on what I believe is an extremely timely equity (delivered via email upon membership), I am offering a limited time $299 annual membership for the first 100 members. To get this discounted price, simply use the coupon code “first100”.

Ultimately, I think we are now at a major inflection point in the financial markets, which has been ongoing in slow motion for three years, but which could suddenly accelerate. Being different, being contrarian, has been extremely painful for a long time now, however, resilience and persistence, two necessary qualities for success in contrarian investing, in my opinion, are leading to what I believe is an upcoming golden age for active investors.

Hope you enjoyed my trip down memory lane as much as I did (I still remember running stairs every morning at the high school football field trying to build up calf strength to dunk a basketball…different worries today),

WTK

Disclosure: I am/we are short spy as a market hedge, and have put more money into commodity equities that i ever should have, yet the opportunity remains IMO.

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.