So far, the bond market has diverged from the stock market, and the commodity market. Most think the bond market is the “smart money”, however, Adam Robinson has proven that this has generally not been the case since 2000, as I shared with my members earlier this week.

What does this mean in practicality?

In simple terms, Treasury Yields could be finally poised to rise materially, particularly at the longer-end of the curve.

What could be the catalyst?

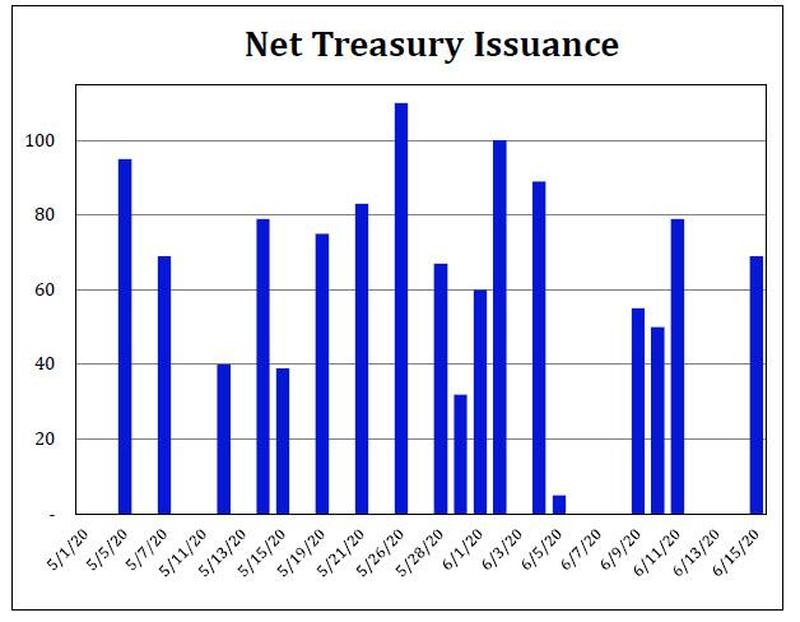

How about new Treasury issuance that outpaces the reduced scope of Fed Treasury buying? This is more probable than it seems, in my opinion, as Fed Treasury buying has gone from a full gusher, at $75 billion per day, to a relative trickle, ending last week with the Fed buying $6 billion in Friday’s trading session.

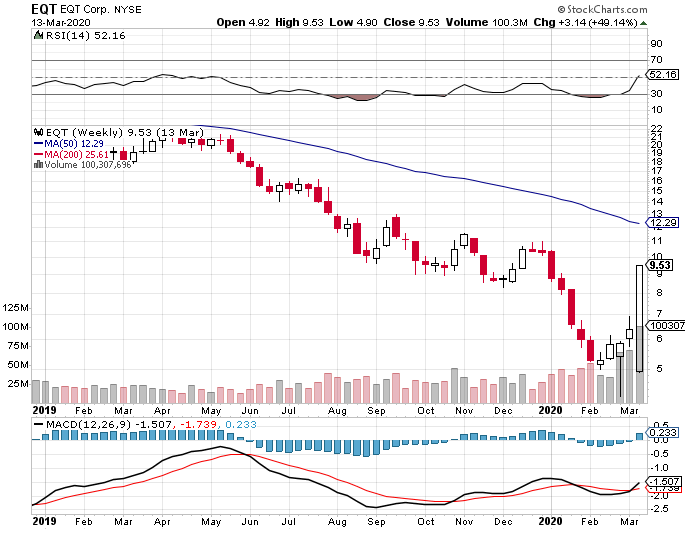

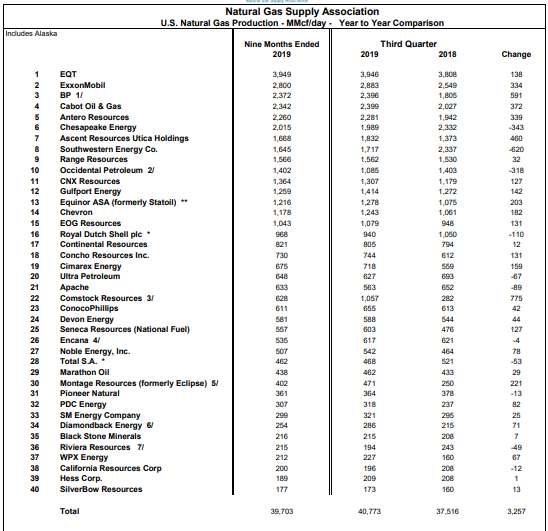

EQT Corp, the largest dry natural gas producer in the U.S., gained 49.1% last week.

Many natural gas equities had stellar performance weeks, while SPY dropped 9.5%, and historic volatility engulfed the markets.

Looking through the volatility, the inflection point is clearly at hand.

Introduction

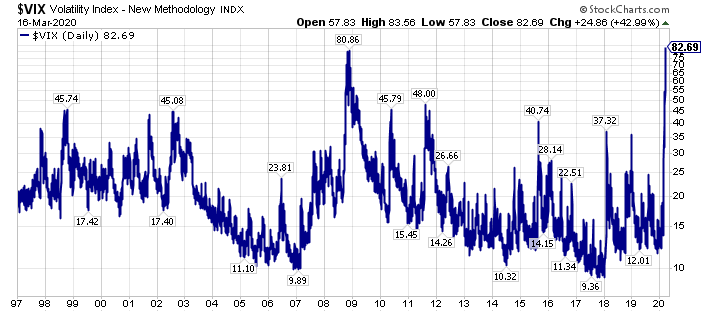

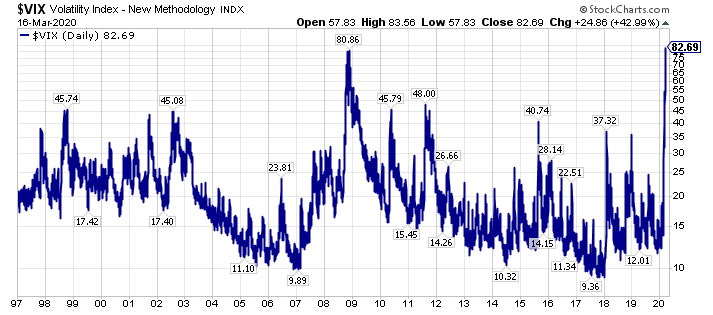

There has been historic volatility in the financial markets. That is not hyperbole, as the chart of the $VIX shows below.

In fact, even though the SPDR S&P 500 ETF (SPY) declined 9.5% last week, we have seen daily price moves, on a regular basis, that exceed that move.

In this swirling sea of turmoil, one sector that I have extremely bullish on stands out.

Specifically natural gas, and more specifically, the historically downtrodden natural gas equities, which have both been contrarian trades and investments even for contrarians.

Dry natural gas prices rose 9.4% last week, the United States Natural Gas Fund (UNG) rose 10.7% last week, and the largest dry natural gas producer in the United States, EQT Corp (EQT), rose 49.1% last week.

Macro Is Turning Sharply To Favor Natural Gas

Anybody that has been reading my work knows that I have been extremely bullish on natural gas prices and natural gas equities.

Why?

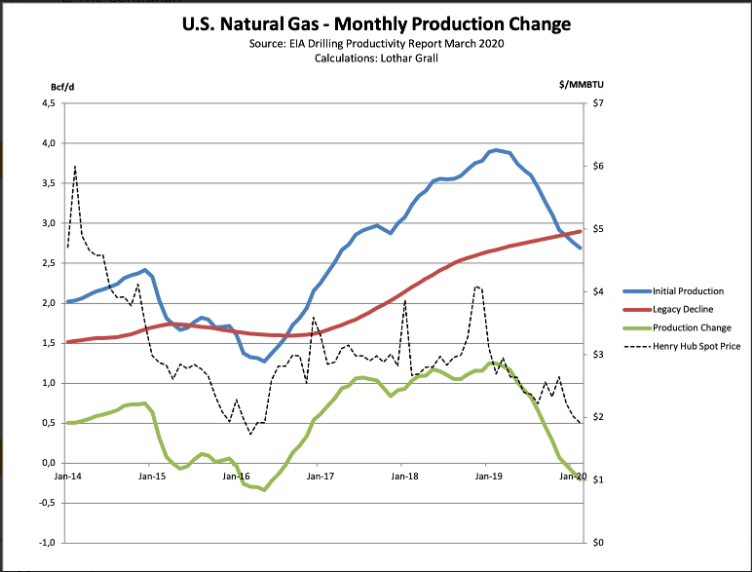

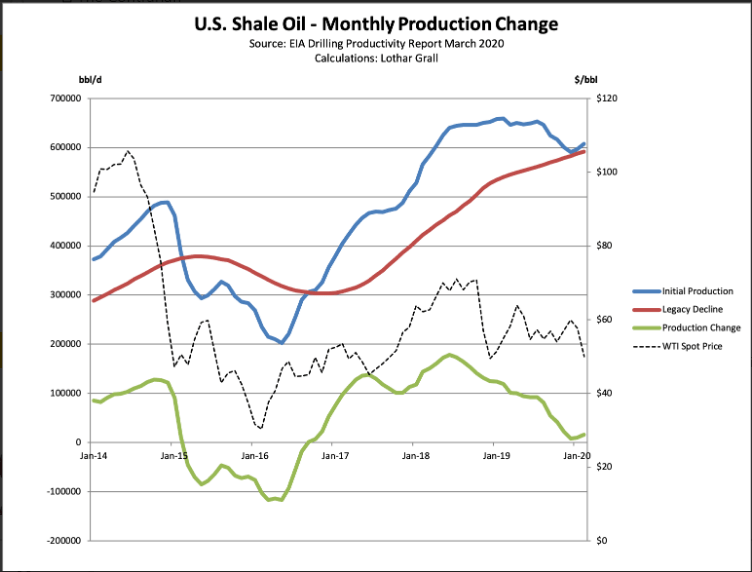

In a nutshell, both lower 48 dry natural gas production and liquids production are rolling over, as the charts of my colleague Lothar Grall illustrate.

(Source: Lothar Grall, The Contrarian)

Keep in mind, this data is from the EIA’s Drilling Productivity Report, and production was already in decline for dry natural gas and rolling over for liquids before COVID-19 became a full blown pandemic, and Russia and Saudi Arabia got into a full scale oil war.

The latter has cratered crude oil prices, and effectively rendered obsolete the primary bearish natural gas thesis, which was that unending associated dry gas production growth would forever impair dry natural gas prices.

Natural Gas Equities Have A Contrarian Surge

Again, last week, with the SPDR S&P 500 Index down 9.5%, the largest natural gas producer in the United States, EQT Corp (EQT), surged higher by 49.1%.

That is a monumental move, in a week of historical market volatility, and adding to the narrative, many of the leading dry natural gas producers had a strong week of relative, and absolute, price performance.

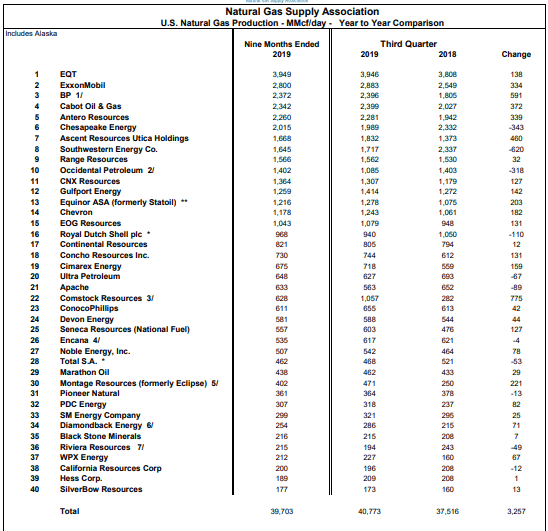

As this narrative begins to flow through to market participants, there is potential for extraordinary gains, perhaps even a generational wealth opportunity, as I wrote about in an article highlighting Antero Resources (AR) recently, in some of the largest dry natural gas producers in the table above.

On this note, much beleaguered Exxon Mobil (XOM), which is widely ridiculed for their XTO energy purchase in 2009, which gave them greater natural gas exposure, could get a material, unexpected (by many market participants) boost from higher dry natural gas prices.

Closing Thoughts – Take Advantage Of What I Think Is A Historic Opportunity

Many always ask me how I had a year like I did from November of 2008 to November of 2009.

The answer was really simple.

1. Have an accurate bigger picture macroeconomic view.

2. Identify opportunities that are mispriced by the markets.

3. Take advantage of the panic selling.

Fortunately, for market participants today, we have all the ingredients necessary for one of the great contrarian inflection points of all-time.

For members of my research services, I have published several recent pieces quantifying the historical volatility and the opportunity as follows:

(Note: Members can click on these articles to access. Also, the first article is still being distributed).

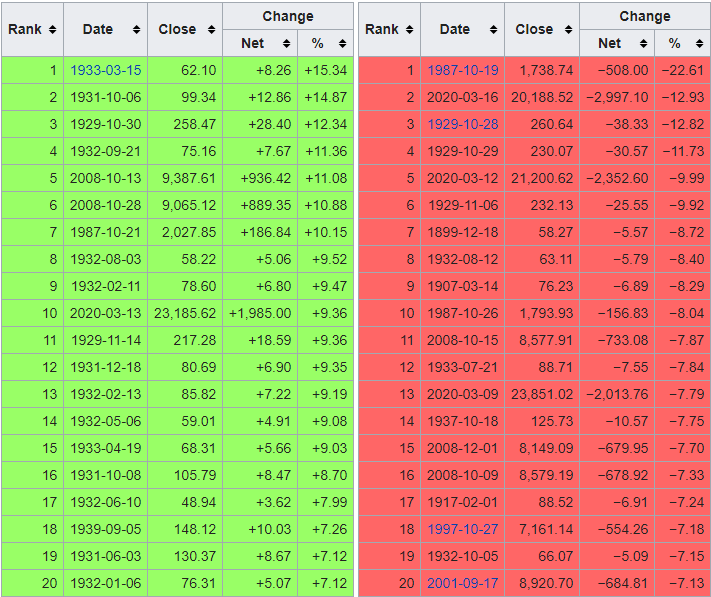

Somewhat unbelievably, we have had three historic days in the stock markets in the past six trading sessions, really four historic days counting Friday’s big gains, so the volatility is incredible.

Seeing through all of this volatility, there are clear inflection points at hand, and the relative and absolute opportunity right now is as big as I have seen in my 25 year plus personal and professional investment career.

In summary, buy what is cheap, and buy into the panic, as the cheapest valuation equities with the best future return prospects will often rebound ahead of a bottom in the broader equity market.

Specific to my research services, I am offering a 20% discount to membership (I am extending this through March) to “The Contrarian” (past members can also direct message me for a special rate), the lowest price point since the founding members price, where we have a live documented history dating back to late 2015.

Additionally, I am offering a limited time 50% discount for the first 10 new members (I expect these slots, some of which I view as a stepping stone to “The Contrarian”, to fill up fast as they have done previously) to a host of research options, including a lower price point. If you subscribe to a premium option (I have had one concierge slot open up), I will set-aside time for a personal phone call to get up to speed. To get these offers, go here, and enter coupon code “opportunity” without the quotes. Either way, once you sign up, I will follow-up with a welcome email within a day.

Reach out with any questions via direct message (I enjoy the dialogue at market inflection points).

Via my research services, or another avenue, please do your due diligence, and take advantage of what I believe is a historic inflection point, which I believe will supersede 2000-2002 in the growth-to-value rotation.

Disclosure: I am/we are long AR, EQT, UNG, XOM, and short SPY in a long/short portfolio.

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.

Panic selling in the broader stock market may have just begun.

Under the surface, panic selling has been ongoing in selected sectors and stocks for an extended period of time.

This presents the historic opportunity.

Introduction

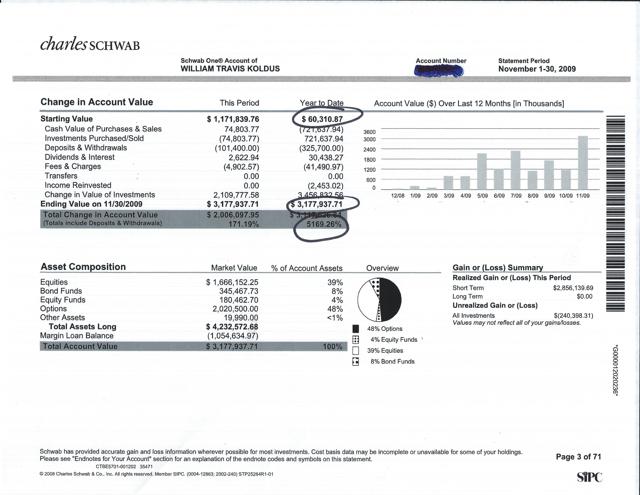

Often, I get the question of how I have achieved out-sized returns (and losses) in the past, particularly with an emphasis on what I have been able to do in my very good years, including 2016, 2003, 1999, 2000, 2008, 2010, and most notably 2009, as illustrated by the snapshot of an aggressive Portfolio that I managed personally for myself below, where I took roughly $60,000 in November of 2008 to over $3 million by November of 2009.

How did I achieve the above returns, over 5000% in a years time (which BTW I may never top, however, knowing this reality, does not stop the pursuit of good years, particularly at inflection points)?

There is a lot of complexity in the answer, including having a variant view, specifically on the broader market as measured by the S&P 500 Index (SPY), using some leverage to express this view, primarily via options, which can be very dangerous tools in inexperienced hands, and the willingness/ability to go against the grain.

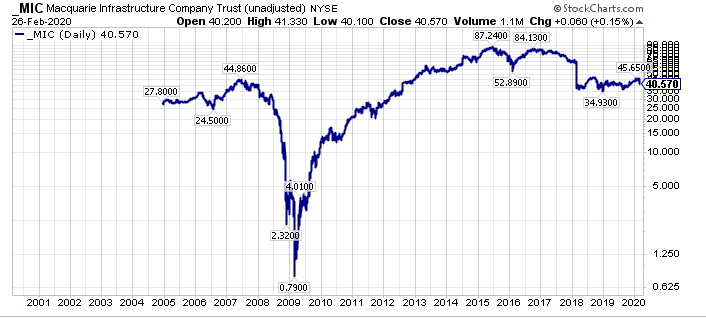

Having said this, there is also a lot of simplicity in the answer, specifically in the main underlying driver of the returns, which was buying significantly out-of-favor equities, with one example being my March 2009 and April 2009 purchases of Macquarie Infrastructure (MIC) for roughly $2 a share. Famously, MIC got down to $0.79 (before dividend adjustments…so I was down roughly 60% on even what I thought were bottom ticking purchases…think about that for a minute) and topped $80 per share, again before dividend adjustments, while also reinstating a substantial dividend, that has been roughly $1 per quarter for some time now (this dividend had been suspended in 2009 before being reinstated).

Clearly, with the benefit of hindsight, purchasing MIC at the lows was a generational investment opportunity, however, it was not easy at the time, even though I had done thousands of hours of due diligence on the company, similar to the focused due diligence effort I have done today, on out-of-favor, undervalued securities.

The key was buying into the panic selling, taking advantage of the panic, and I think we are seeing similar levels of opportunity today, just not in the places that most investors want to look.

Buying Into The Panic

In my November 2008 to November 2009 example above, I actually started buying what I felt were the most distressed, highest return potential candidate equities in 2008, in the heart of the panic. Remember, the broader equity market did not bottom until March of 2009, which is a whole other story, however, the important point is that some of the most downtrodden equities made their lows prior to the broader market making its lows.

One specific example, is General Growth Properties, the former second-largest mall REIT in the U.S. behind Simon Property Group (SPG), that was eventually acquired by Brookfield Property Partners (BPY) in 2018.

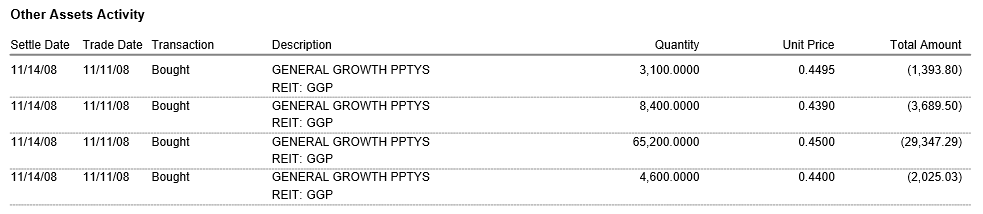

In November of 2008, I was on a due diligence trip through South Florida, meeting with hedge fund managers, and asset managers, and after a legendary night out for this generally non-party owl author (ask me for details if you want), I awoke in my Miami Beach hotel room, looking out at the ocean, and taking in the panic, eventually buying 120,000 shares of GGP on November 14th, 2018 for this specific account, as my brokerage account statement shows (if you want additional details send me a direct message).

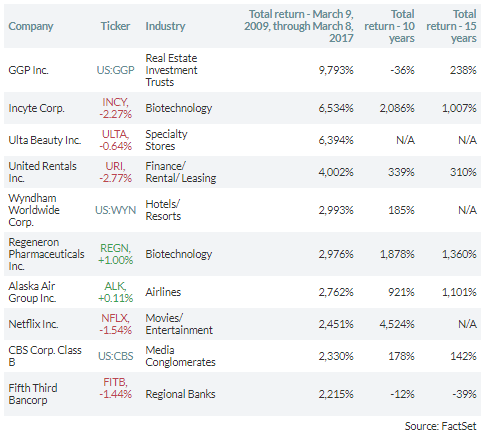

These purchases, in aggregate, totaled $53,593.71, which was not a big dollar total in aggregate, however, the 120,000 shares were a nice stake in what would become the best performing S&P 500 equity in the bull market, at least through March 10th, 2017, as this CBS MarketWatch article on the bull market turning 8 years old chronicled.

In March of 2018, in the Brookfield Property Partners deal, these shares could be exchanged for $23.50 in cash.

Not a bad return at all, however, the key was to buy into the panic.

Where Is The Panic Today

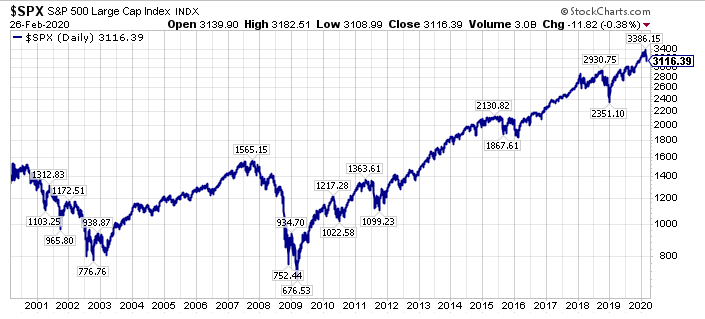

Even though the S&P 500 Index is on track to be down 7% or more this week, as I write this post, the real panic is not in the broader stock market, at least not yet.

In fact, on a long-term chart, the recent decline is just a blip.

Now, we could be on our way to a broader stock market sell-off, as GMO has previously outlined earlier in 2018.

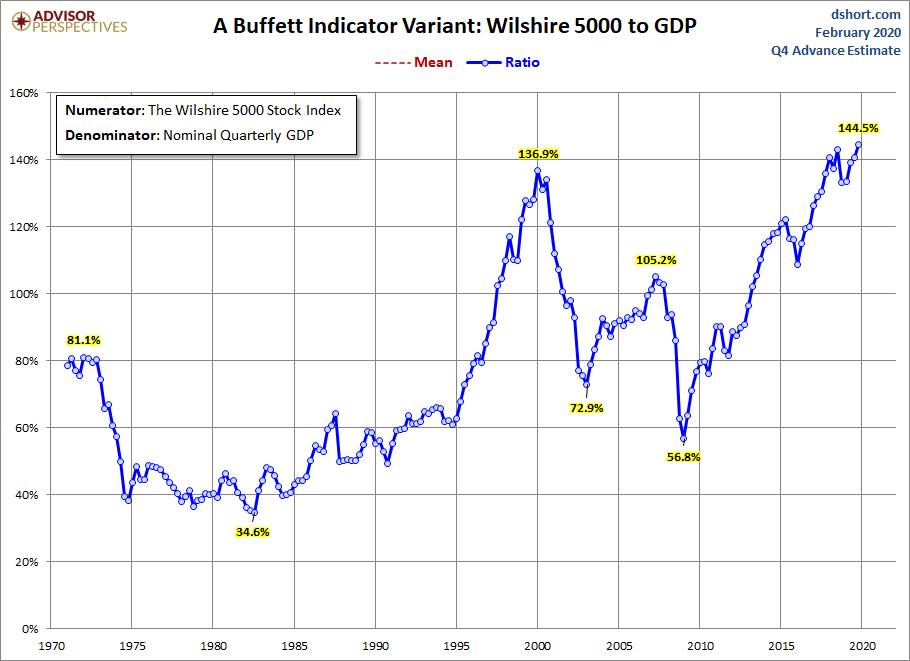

Regarding the path of the broader markets, that is yet to be determined, as we grapple with historically extended valuations, and historical monetary policy accommodation levels.

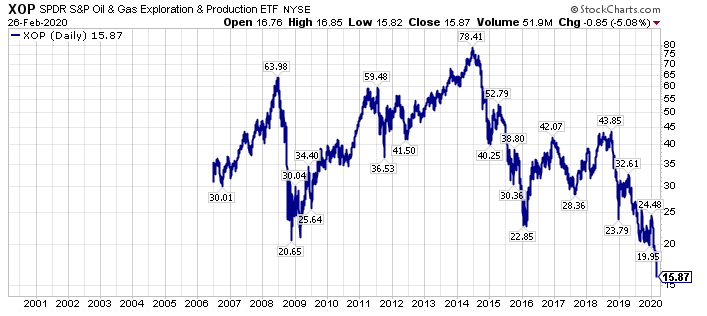

The real panic right now is in the underbelly of global economic activity, specifically in economically sensitive cyclical stocks, and more specifically, in the most loathed of all stock market sectors today, which is of course, the energy sector.

The SPDR S&P Oil & Gas Exploration & Production ETF (XOP) offers a glimpse of this panic, with XOP down 79.8% from its 2014 high, and down 63.8% from its 2018 high.

Thus, with the broader U.S. stock market, as measured by SPY, only down roughly 8% from its recent highs, the compare & contrast should be eye opening for most investors.

Building on the narrative, with our deep research dives, we feel there are a number of out-of-favor equities that are down even greater in percentage terms, which offer even greater relative and absolute opportunity.

Importantly, similar to several of the downtrodden equities I purchased in late 2008, and early 2009, including General Growth Properties, and Genworth Financial (GNW), which was also bought well below $1 in November of 2008 before shares rebounded above $18 by early 2010, the most out-of-favor, undervalued equities right now, will probably bottom ahead of the bottom in the broader equity market.

Panic Selling Is Yielding Opportunity

It is no secret that I am targeting what I believe are the most undervalued securities, with the goal of creating a generational wealth opportunity. These securities are generally loathed, unloved, and scorned right now, and many of these equities would make your stomach turn looking at long-term charts, part of the reason there is so much opportunity.

While the best opportunities are generally in smaller capitalization names, there is opportunity in large-caps, including in energy stalwarts like Exxon Mobil (XOM), Occidental Petroleum (OXY), and Schlumberger (SLB), all of which offer attractive yield-oriented income opportunity.

These three securities are part of a “Stuck On Yield” Model Portfolio, which is a $100,000 portfolio, that I created on Friday, February 21st, for a family member.

This Portfolio is yielding over 14% right now, and I have done deep-dive due diligence on all its member components, a majority of which are from the target rich energy sector.

Members of The Contrarian can see this Model Portfolio here, and I have sent out emails of this Portfolio to members of my research services, and I will be making it available this week for all my research members.

Closing Thoughts – Be Ready To Buy Now

Nobody, including me, really knows where the stock, bond, and commodity markets are headed right now with certainty. All we have is probabilities, and ultimately, our valuation analysis. The latter is crucially important, as buying the most undervalued assets, ultimately leads to the strongest returns, so long as you can ascertain the underlying asset quality, and survivability of the corporate entity.

On this note, I am going to make mistakes, so the key is getting a handful of these right, as the gains from the survivors will more than make up for any losses, at least that is my past experience at previous inflection points. Ultimately, valuation matters, and starting valuations levels matter too. Adding to the narrative, with everyone wanting to own quality today, there are many “Have Not” securities that are historically undervalued.

Conversely, a high valuation is a bad starting point, and buying overvalued assets, which certainly describes the S&P 500 Index, which trades at greater EV/EBITDA, Price/Book, and Price/Sales multiples that it did at its peak valuation levels in late 1999/early 2000, is a recipe to achieve poor returns going forward. Adding salt to the wound, the bond market, which offers meager sovereign yields, is also set-up for poor future returns over the longer-term, as historically over 90% of bond returns are correlated with starting yields.

In summary, buy what is cheap, andbuy into the panic, as the cheapest valuation equities with the best future return prospects will often rebound ahead of a bottom in the broader equity market.

Specific to my research services, I am offering a 20% discount to membership (I am extending this through March) to “The Contrarian” (past members can also direct message me for a special rate), the lowest price point since the founding members price, where we have a live documented history dating back to late 2015..

Additionally, I am offering a limited time 50% discount for the first 5 new members (I expect these slots, some of which I view as a stepping stone to “The Contrarian”, to fill up fast as they have done previously) to a host of research options, including a lower price point. If you subscribe to a premium option (I have had one concierge slot open up after a gentleman I was speaking to last evening held off on taking this slot), I will set-aside time for a personal phone call to get up to speed. To get these offers, go here, and enter coupon code “opportunity” without the quotes.

Reach out with any questions via direct message (I enjoy the dialogue at market inflection points).

Via my research services, or another avenue, please do your due diligence, and take advantage of what I believe is a historic inflection point, which I believe will supersede 2000-2002 in the growth-to-value rotation.

Disclosure: I am/we are long MIC, OXY, SLB, xom and short spy in a long/short portfolio.

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.

This is just a short post to document something remarkable.

Volatility is actually above 2008’s high levels.

With the Dow Jones Industrial Average (DIA) posting is second worst percentage decline ever, and a cluster of recent days on the worst performing days list, perhaps the jump in volatility amid the COVID-19 pandemic should not be a surpise.

Adding to the narrative, the S&P 500 Index (SPY) posted its third worst percentage decline day ever.

Ultimately, volatility is opportunity, and this elevated volatility will not be around forever. Thus, I think market participants should be making their shopping lists for what to own on the long side.

I have been waiting for a long time for a set of events to end the virtuous melt-up, fueled by passive and ETF fund flows.

Coronavirus could be the black swan that causes a reversal of these fund flows.

Non-correlated equities with low index representation stand to benefit disproportionately.

Introduction

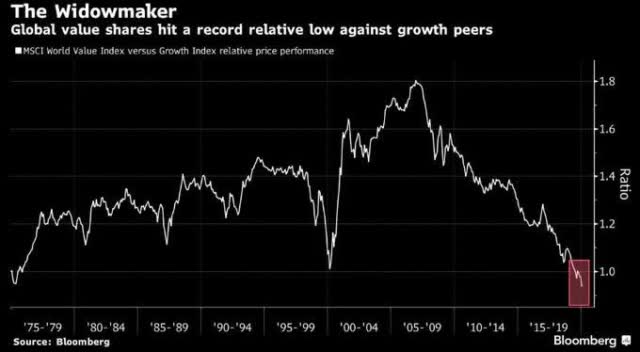

We are potentially on the verge of an historic capital rotation from growth to value, sparked by black swan catalysts that nobody envisioned a short time ago.

Building on this narrative, on February 6th, 2018, I wrote one of my most popular articles published on Seeking Alpha titled, “Be Prepared For A Crash – Part II“, and in the article, I specifically investigated the lack of price discovery in the markets, as passive, ETF, and dividend growth fund flows were largely price insensitive and valuation insensitive in their endless buying.

Today, that virtuous, seemingly never ending cycle has the potential to work in reverse fashion. In Steven Bregman’s words, all that was needed was a signal event to jump start a golden age for active investors, and we may have one transpiring in real time.

To illustrate this point, I referenced several quotes from Steven Bregman, president and co-founder of Horizon Kinectics, who presented at James Grant’s October 4th, 2016 Investment Conference.

Here is the first set of quotes I referenced:

“A golden age of active investment management awaits only one signal event, Steven Bregman, president and co-founder of Horizon Kinetics, told the Grant’s conference-comers on Oct. 4. A collapse of the index/ETF bubble is that intervening disaster. To hear Bregman tell it, no crash would be so well-deserved

He called the exchange-traded fund excrescence the world’s biggest bubble.

“It has distorted clearing prices in every sort of financial asset in every corner of the globe…,” asserted Bregman. “[I]t has created a massive systemic risk to which everyone who believes they are well diversified in the conventional sense are now exposed.”

I could not agree more with the statement quoted above, and these price distortions have increased at an exponential rate from 2017-2019, and early into 2020, as crowded trades have become more crowded.

Conversely, the “Have Not” equities have been shunned to an even further degree, creating the most bifurcated market that I have seen in my 25 plus years actively investing and speculating.

A Historic Capital Rotation Is On The Horizon

Once passive, ETF, and index fund flows reverse, the disproportionately beneficiary equities, think the leading market capitalization index favorites, are going to be the equities that are hurt most by the reversal of fund flows. Conversely, out-of-favor equities that have been shunned, will actually benefit, as long/short funds reduce gross market exposure, and net buying, at least net relative buying will head to these equities.

On this note, here are the 25 largest components of the SPDR S&P 500 Index ETF (SPY), which have all been buoyed by never ending passive fund flows.

Personally, I think the top weighted companies on this list, which dominate the S&P 500 Index, and the Invesco QQQ Trust ETF (QQQ), have a chance to sell-off dramatically, if a true capital rotation takes hold from growth to value.

Given the current extended levels of growth versus value, there is a ripe opportunity for an epic price reversal.

Looking at the above, look how steep the price reversal was in 2000-2002, with the growth to value relationship reversing on a dime, and moving straight in the other direction.

Could the same thing happen today?

Yes, is my unequivocal answer, partly because the in-favor investment strategies and trades, think passive, ETF, and dividend growth fund flows, are even more popular today on a relative basis than they were in the late 1990’s, as almost every registered investment advisor in the U.S. has shifted to some form of passive indexing.

Wrapping up, coming from a value investment background, I have seen many of my peers ground to dust, and legendary value investors essentially take their ball and go home. Personally, I have more significant scars from this time frame than any other.

The collective price action and collective investor response is very reminiscent of Julian Robertson closing his Tiger Funds near the exact peak of the 1990-2000 bubble, an investment landscape that had seen Warren Buffett routinely criticized. Of course, this was followed by a massive reversion-to-the-mean trade from 2000-2002, and really 2000-2007, where value investing handily outperformed.

Building on this narrative, during 2000-2002, the S&P 500 Index lost roughly 50% from peak-to-trough, while many value stocks, including REITs, like Realty Income (O), which was loathed at the time, but loved today after roughly two decades of out-performance, surged higher, even with the broader market struggling mightily.

With that last thought in mind, consider what investments are loathed, and loved, today.

In closing, for the value investors that are left today, the odds seem insurmountable, however, the opportunities, particularly on a relative basis, are as big as they have ever been.

To get an idea of how I am positioning for this opportunity, since we are past there, in my opinion, I am offering a 20% discount to membership (I am extending this through February) to “The Contrarian” (past members can also direct message me for a special rate), the lowest price point since the founding members price, where we have a live documented history dating back to late 2015..

Additionally, I am offering a limited time 40% discount for the first 5 new members, repeating a successful promotion from earlier this month (I expect these slots, some of which I view as a stepping stone to “The Contrarian”, to fill up fast as they have done previously) to a host of research options, including a lower price point. To get this offer, go here, and enter coupon code “february 2020” without the quotes.

Reach out with any questions via direct message.

Via my research services, or another avenue, please do your due diligence, and take advantage of what I believe is a historic inflection point,

Disclosure: I am/we are long BAC, C, xom, and short AAPL via put options and spy in a long/short portfolio.

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.

As coronavirus fears spread, potentially triggering the signal event that ends the seemingly never ending, passive fueled price insensitive and valuation insensitive buying binge, how low can U.S. long-term interest rates go?

U.S. longer-term interest rates seem to already be pricing in a worst case, low growth, low inflation environment forever scenario.

Said another way, maybe the market is not prepared for a different investment landscape developing.

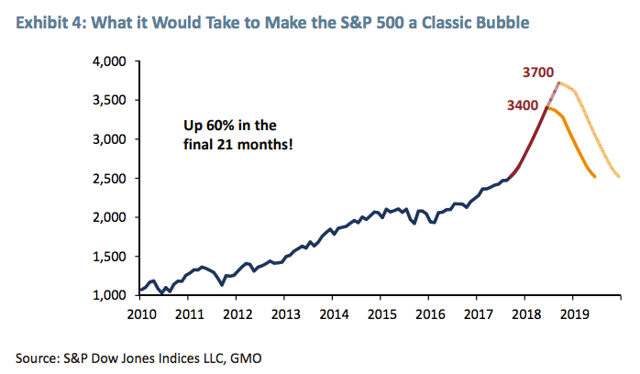

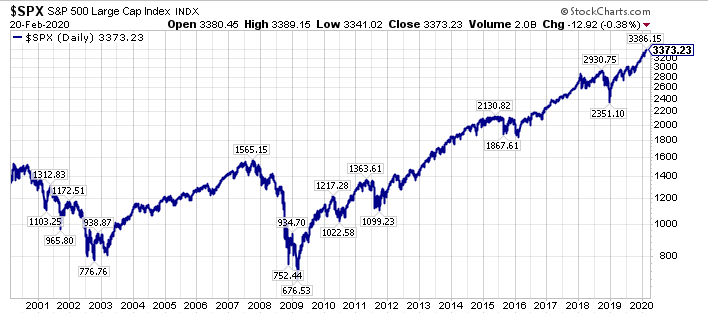

We have clearly followed the path of the classic bubble that GMO laid out in 2008 for the S&P 500 Index ($SPX), (SPY), which is shown below.

The timeline has been slightly different, I call it an extended classic bubble, the slower ride to the final destination. Regardless of the course, we are here now.

The key question is where do we go from here, and the answer, from my perspective, is all a function of interest rates, particularly longer-term sovereign interest rates. With the yield curve close to inverting again, and two Fed Funds rates cuts priced in right now as of this writing (February 21st, 2020) through the December 2020 FOMC meeting, a lot of pessimism is priced in.

Additionally, sovereign interest rates are so low, the question needs to be asked, “How much could they go down in the next recession?”

Last, but not least, what if a recession is averted, or we experience a mild recession, similar to what happened in the midst of the 2000-2002 bear market. On this note, the current investment landscape reminds me an awful lot of late 1999/early 2000, with the moonshot blow-off in Tesla ($TSLA), and the greater concentration in the top-five S&P 500 names ($SPY), which are Apple ($AAPL), Microsoft ($MSFT), Alphabet ($GOOGL), ($GOOG), Amazon ($AMZN), and Facebook ($FB) than in late 1999/early 2000.

We all know how that story ended, however, almost all market participants have forgotten that 2000-2002 time frame, hyper-focused on a fear of a reprisal of 2007-2009, which has led us to where we are today.

And where is that, you may ask?

The answer is that we are on the cusp of a historical capital rotation. Stay tuned.

Earlier today, a public article I posted about Antero Resources (AR) was published on Seeking Alpha. You can find it under this title & link, “Antero Resources Is A Generational Buy: Dispelling The Myth Of Antero As A High-Cost Producer“. While writing this article, and spending a lot of time researching commodity equities, and more specifically energy equities the past 5 years, really the past 7 years, that has snowballed to an almost obsession now, due to the inherent undervaluations, I have slowly worked to the conclusion that most market participants have become over obsessed with quality and/or perceived quality.

What do I mean by this?

In the case of Antero, almost all long/short fund managers I know, are long Cabot Oil & Gas, and short Antero. The relentless price action in favor of this trade, has essentially eradicated valuation sensitive and price sensitive money out the door.

Building on this narrative, the Darwinian survival funnel of the markets, has led almost all investors to the same securities the past decade, a ending place where quality and dividends are praised above all, and the perceived quality, and sustainability of dividend growth, and/or yield is worshiped.

The end result of this process is a bubble that is bigger than the late 1990’s bubble, more pervasive, and more driven by longer-term sovereign interest rates than anything else.

Looking back to 2018, GMO laid out a path for a classic bubble for the S&P 500 Index (SPY), and we are there, as the following graphic illustrates.

Looking at the above, once we peak, and roll-over, the path is frightening, something many market participants have some how forgotten following 2007-2009, and 2000-2002.

Really, though, it is worse than that, as yield-oriented investors have been pushed out the risk curve, and the perceived quality equities, namely the dividend payers, have become essentially the longest duration bonds.

Jumping straight to the punch line, what happens when almost all market participants embrace quality, perceived quality, and are piled into essentially the longest duration assets, chasing yield, when longer-term interest rates rise?

Who is prepared for this?

Will this lead to the historic bifurcation between the “Have’s” and the “Have Not’s” being closed?