(Travis’s Note: This article was originally published on January 17th, 2018, and I am re-posting today, October 28th, 2018 to add to the archives, and remember the challenges of 2017 as a Learning Lesson).

- I have learned more in life through my failures than my successes.

- 2017 was an excruciating, challenging year and I made significant, critical mistakes.

- Capital was destroyed, which is precursor for what the broader market is going to do to many investors from today’s valuations.

“We all go through trials and tribulations, and when you see how a person handles it, that really says a lot.”

– Chris Mullin

While most investors and speculators celebrated a fortuitous 2017 in the investment markets, I managed to have one of the worst years relatively, and absolutely, that I have had in my two decade plus career actively investing & speculating. It was made even more painful, by the fact that this occurred after our terrific 2016, when it appeared that out-of-favor, value-oriented equities turned the corner in significant way.

The non-stop, relentless rise in the broader investment markets, specifically the S&P 500 Index (SPY), which only trades up nowadays, poured salt in the open wound, and all year, it felt like I was fighting uphill, which was the opposite of the remarkable reversal and rebound that we captured in 2016.

Looking back, I made clear, significant mistakes, and I severely, negatively impacted the investment portfolios of people close to me, destroying capital, which has to be one of the worst feelings in the world.

The silver lining to this unexpected turn of events is that I have found in life, that I learn more from my failures than I have from my successes, even the significant ones that I have been fortunate to enjoy (I have had my share of significant challenges too).

Specifically, I have found that, through failure, you learn more about relationships than you do in success, as successes can paper over cracks, fault lines, or real feelings, while failures tend to spur a “circling of the wagons” for those that are truly close to you, which makes eventual victories sweeter when/if they do occur.

On that note, I am very thankful for the members of “The Contrarian“, and everyone I work with directly and indirectly, as we continue to build a special community of members that aims to take advantage of historic price anomalies in the investment markets.

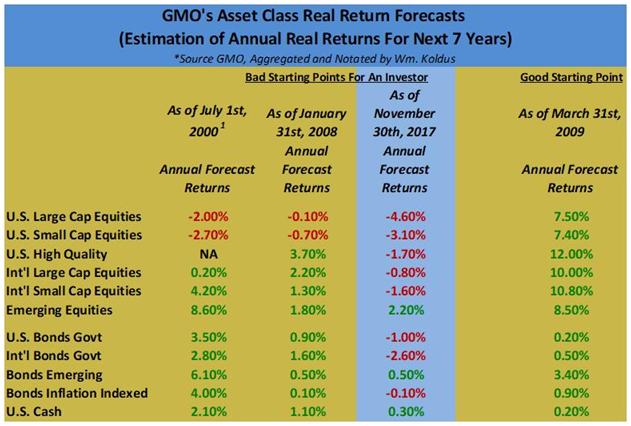

In summary, as a market historian, I have rarely seen price dislocations like we see in today’s markets.

Frankly, the price dislocations today rival the greatest price anomalies in modern market history, including the important calendar dates of 1929, 1973, 1999, and 2007.

Reading that and inferring from the dates mentioned, you may think that I am only focused on the downside, which is significant, but that is only partially true. There are enormous upside opportunities too, as both long and short trades are enormously crowded right now, in my opinion.

Given today’s valuations, most investors, in traditional stock and bond portfolios, would be better going to cash (where short-term interest rates will rise) and taking a five-year vacation, checking in periodically, perhaps once a quarter, for better buying opportunities. I will write more about this in the future, as it is the least I can do to preserve capital.

To close, in a picture, this is how I felt about 2017.

Looking forward to 2018, and moving forward from a despondent, depressing year (entirely of my own doing), where almost all common sense with regard to valuations has been thrown out the window.

Thank you for reading, and please be mindful of the rare investment environment that we are in today,

WTK

Disclosure: I am/we are short SPY as a Market Hedge.

Additional disclosure: Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.