(Travis’s Note: This article was originally published on July 16th, 2017, and it is being re-posted today, October 28th, 2018, to organize for the archives. Long/short has had a very difficult past decade, but I believe it is primed for a very good decade ahead).

The past several days, I have been working on an article for members of “The Contrarian”, that reviews a generational hedge fund call from 2013, and why this call remains relevant today.

In going through my archived writings, I came across an article I wrote on long/short investing in January of 2016, and I wanted to highlight a portion of that article, specifically my comments on long/short investing.

Here is the excerpt from the January 2016 article:

Reflection On My Long/Short Investment Philosophy

Ever since I learned about Alfred Winslow Jones, the pioneer of hedge fund investing, I was fascinated by the long/short investment strategy. Ideally, it performed well in up- and down-market environments, and separated stock picking skill from general market movements.

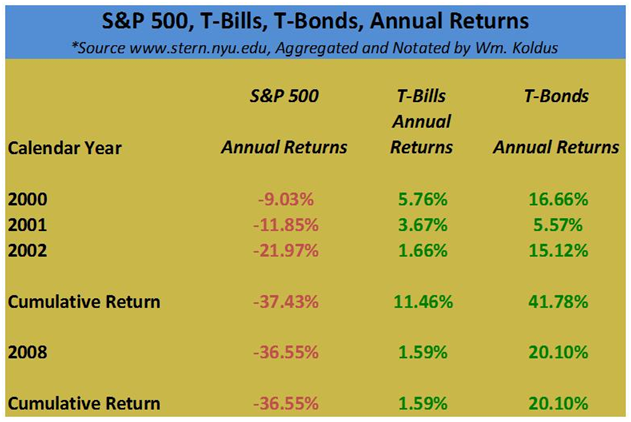

During my early career as an investment analyst, I focused on value-oriented investment managers and their philosophies. Some of my favorite investment managers were Mason Hawkins, Marty Whitman, Bob Rodriguez, Dan Fuss, and Jean-Marie Eveillard. Reading their analysis and following their investment strategies influenced and shaped my thinking. The 2000-2002 time frame reinforced my value leaning, as value managers, especially the aforementioned ones, strongly outperformed, as the S&P 500 Index declined nearly 40%.

In contrast to 2000-2002, the dramatic downturn of 2008 treated value investors far differently. Many value investors piled into financial stocks as they declined, attracted by the relatively and historically cheap valuations. Trying to buy value investments in 2008 was akin to catching a falling knife, similar to buying commodity stocks over the last three years (Author’s Updated Note: commodity stocks had a historic reversal and rebound in 2016), and many value-oriented investment investors and firms went out of business.

The tremendous volatility of 2008 also negatively impacted long/short equity hedge fund managers. From my perspective covering hedge fund managers at the time, many long/short portfolios experienced historic volatility and drawdowns, especially in the second half of 2008, particularly in the months of October and November. Observing how these managers responded, reducing gross and net exposure, and emphasizing their highest conviction investments, was an invaluable learning experience.

During 2008/2009, I kept my eyes fixated upon the performance of a select few hedge fund managers. One firm that I followed closely for personal and business reasons was Lee Ainslie’s Maverick Capital. Lee Ainslie, one of my favorite investors, is a descendant in the lineage of the legendary Julian Robertson (another one of my favorite investors), and he sparked my curiosity with how his team structured Maverick’s portfolios. Maverick was founded in 1990, and since inception, it has focused on long/short equity investing, eschewing macro, currency, and interest rates bets.

Part of my attraction to Maverick’s investment philosophy was that it was different from my own investment philosophy. Personally, I have always liked macro forecasts and the trading and investing opportunities that they inspire. My strong 2008 and 2009 performance years were largely the result of my macro market views. Because of their love for macro investing, I have been drawn to investors like Stanley Druckenmiller or John Burbank of Passport Capital, and they have heavily influenced my investment philosophy.

To summarize, value investing, long/short investing, macro calls, and a general contrarian stance have all become critical components of my personal investment philosophy. The struggles I have endured trying to buy historically cheap commodity stocks over the last several years has scared me, and caused me to at least consider a worst-case scenario more than I did prior to this experience (Author’s Updated Note: It has also caused me to heavily research the capital cycle, and members of The Contrarian will know what I am referring to specifically).

The resulting compilation of investment philosophies has been mashed together to produce the Contrarian All Weather Portfolio, my version of a long/short portfolio (Author’s Updated Note: This portfolio has has material out-performance since its December 7th, 2015 inception despite the robust performance in the U.S. stock market). At its heart, stock-picking results, netted out by a SPDR S&P 500 ETF (SPY) hedged position, will drive the returns of the portfolio. A majority of the individual stock selections are value oriented in some fashion. Additionally, there will be a macro theme to the portfolio alongside some macro positioning at the margin.

Takeaway: Long/Short Investing Is More Timely Today

Similar to the late 1990’s, which culminated in a period where growth outperformed value for roughly ten years, the past decade has also seen growth outperform value ironically from 2008 through today, in an environment where stock and bond valuations have become historically extended.

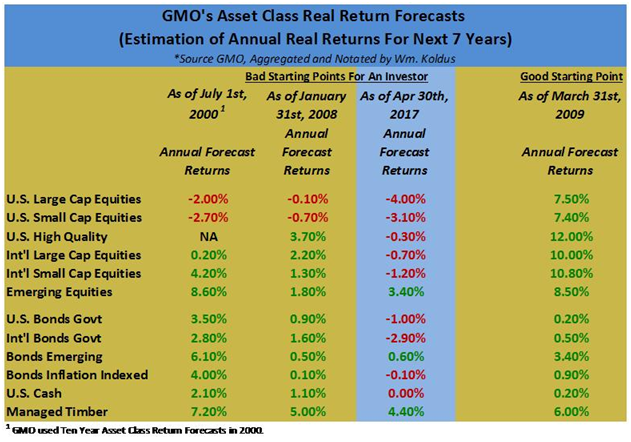

The end result is that expected future real returns today, for both stocks and bonds, are some of the lowest projected real returns in history.

Additionally, with bond yields low in nominal terms, the next significant market correction in U.S. equities, will not see investors saved by bond out-performance, in my opinion.

To close, there is a high probability that a traditional “60/40” equity/bond portfolio or “70/30” equity/bond portfolio will have negative real returns over the next decade. All investors should think about today’s starting valuations when constructing their portfolios.

William “Travis” Koldus

Disclosure: I am/we are short SPY.

Additional disclosure: SPY short is a hedge position to offset long investments in a long/short portfolio. Every investor’s situation is different. Positions can change at any time without warning. Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies’ SEC filings. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice.